Food System Decoupling?

Could geopolitics help the planet by shortening food system supply chains?

Will food supply chains be the next to decouple and join the ‘friend-shoring’ trend?

We have seen a number of supply chains decouple over recent years due to rising international tensions. With the added stress of the covid pandemic, some commentators have started to suggest that the drive for globalisation is going into reverse.

Food supply chains are coming under heavy stress due to the conflict in Ukraine building on an already high inflation environment. This has pushed food security to the top of national agendas, alongside energy. We explore whether this will result in a food supply chain decoupling and a shift towards shorter supply chains and ‘friendly’ jurisdictions (‘friend-shoring’).

There has been a consistent view that shorter supply chains are more environmentally friendly. Academics estimate that that food miles account for 5% of total food system emissions.1 Maybe this will be a situation where a geopolitical supply chain trend actually benefits the planet.

Decouplings and ‘Friend-shoring’

Friend-shoring – geopolitics and trusted trade partners

Janet Yellen summarised the move towards ‘friend-shoring’ in a recent speech:

‘First, we need to modernize the multilateral approach we have used to build trade integration. Our objective should be to achieve free but secure trade. We cannot allow countries to use their market position in key raw materials, technologies, or products to have the power to disrupt our economy or exercise unwanted geopolitical leverage. Let’s build on and deepen economic integration and the efficiencies it brings—on terms that work better for American workers. And let’s do it with the countries we know we can count on. Favoring the “friend-shoring” of supply chains to a large number of trusted countries, so we can continue to securely extend market access, will lower the risks to our economy, as well as to our trusted trade partners.’ 2

But the political drive set out by Yellen is not new. What began in the tech sector has been playing out more recently in energy and shows signs of spreading to other areas such as lithium.

High tech decoupling

Decoupling of Western and Chinese technology accelerated during the Trump presidency with the imposition of technology export restrictions, import tariffs and restrictions on Chinese companies from participating in 5G infrastructure.

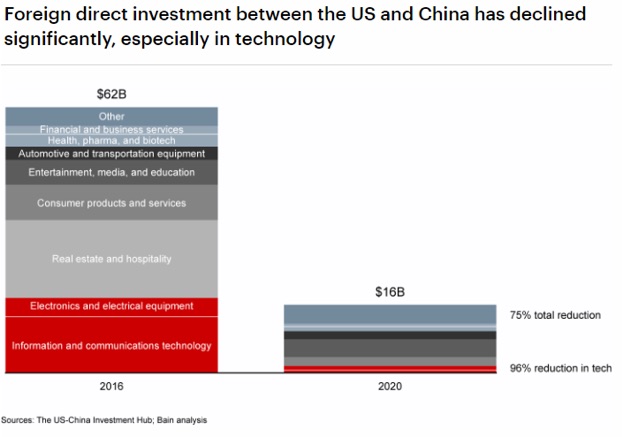

Technology-related foreign direct investment between the two countries dropped by 96% from 2016 to 2020 – see Figure 1.

However, while part of President Trump’s narrative was around technology re-shoring and jobs creation in the US, the main driver in the US (and other western democracies) has been national security concerns and the desire to retain leadership in the most advanced technologies. Russia’s invasion of the Ukraine is likely to add momentum to these concerns.

Figure 1: Foreign direct investment between the US and China has declined, especially in technology

Battery supply chain decoupling – Lithium

A similar debate is occurring with regard to lithium, which is a core component of the batteries that power electric vehicles (EVs). Rio Tinto predicts demand for lithium will grow by 25 to 35% a year for the next decade due to the rising demand for electric vehicles, with both governments and car manufacturers setting lofty goals for the production of EVs.

Currently, the majority of lithium mined in Argentina, Australia or Chile is sent to China to be processed into battery-grade lithium so it can be used in cars or for other energy storage products. China currently controls 59% of processing plants, the United States 4% with Europe having no major plants.5

The political drive to change this is clear. The US Secretary of Energy stated in the National Blueprint for Lithium Batteries that “Establishing a domestic supply chain for lithium-based batteries requires a national commitment to both solving breakthrough scientific challenges for new materials and developing a manufacturing base that meets the demands of the growing electric vehicle (EV) and stationary grid storage markets”.6

Energy decoupling – LNG and Oil

In contrast to technology and lithium, supply chains in the energy market have not previously been talked of in the context of ‘decoupling’ because there has been a clear geographic logic underpinning the transport of oil and, particularly, gas.

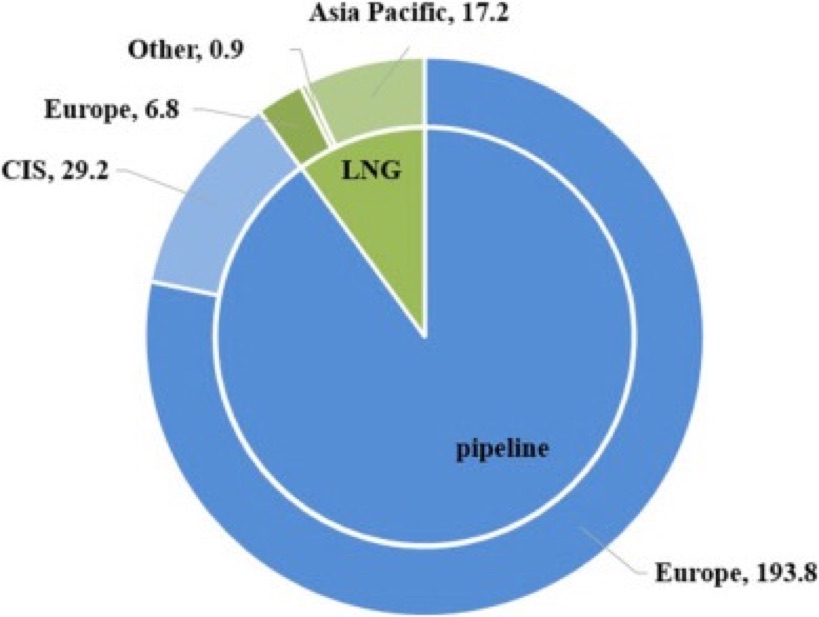

For example, Russia’s routes to market for its gas are very limited, mainly consisting of pipelines to European countries – see Figure 2.

Figure 2: Russia’s gas exports (destinations and methods) in 20187

But Russia’s invasion of the Ukraine has resulted in politics taking priority over geographic convenience in supply chain terms leading European countries to look for alternatives in what could amount to a permanent decoupling of the European energy system.

Transparency and traceability are gradually shifting companies to shorter supply chains

Companies tend to be more agnostic when it comes to trading with partners in different countries and are often slow to react, waiting for their home states to force changes through regulations and/or sanctions.

However, the recent Covid pandemic has revealed the risks inherent in longer supply chains and the public reaction to the Ukraine invasion has shown how swiftly supply chain sourcing can become an issue. These events, combined with the fact that greater transparency is essential if companies are to meet their climate and nature goals, is leading many to look for ways to shorten their supply chains.

A McKinsey survey of 70 respondents in May 2020 found that 93% planned to make their supply chains ‘more flexible, agile and resilient’. A follow-up survey 12 months later found that 92% of the respondents had made changes to the physical footprints of their supply chains and almost 90% expect to pursue some degree of regionalisation during the next three years.8

In addition to increased resilience, shorter supply chains are easier to monitor, allowing companies greater control of sustainability risks such as slave labour, GhG emissions and biodiversity loss as well as more traditional business risks such as fraud.

Planet Tracker’s recent report (Lifting the Rug) on the benefits of traceability systems in the textile industry showed that companies could also reap financial benefits from implementing traceability systems across their supply chains, with an average profit increase of between 3% and 7%. We found a similar result in the seafood industry where traceability increased margins from 3% to 6% (Traceable Returns).

Reducing risks and enhancing profits is an attractive combination, suggesting that companies across multiple sectors will look more closely at restructuring their supply chains in the future.

Will food supply chains rapidly decouple?

There is little doubt that the global food system is already subject to similar geopolitical decoupling pressures as the energy or technology systems, particularly driven by the desire for greater ‘national food security’. Countries have debated how best to achieve this for many years, but the Ukraine crisis has pushed this debate front and centre.

Some exporters have added to the pressures by imposing restrictions. The Food Export & Fertilizer Restrictions Tracker Analysis published by the IFPRI shows that the global share of calories impacted by export restrictions is higher now (at 16%) than it was during the 2008 food price crisis.9 See our blog on The Politics Of Food Protectionism, Nature Dependency And Hunger for further discussion on the importance of a country’s politics when examining the trade of essential food commodities.

Our latest analysis of how different countries are behaving with respect to food exports provides a granular perspective. In ‘The Politics of Food Protectionism, Nature Dependency and Hunger’, we highlight that ‘non-democratic’ regimes are more likely to impose trade barriers.

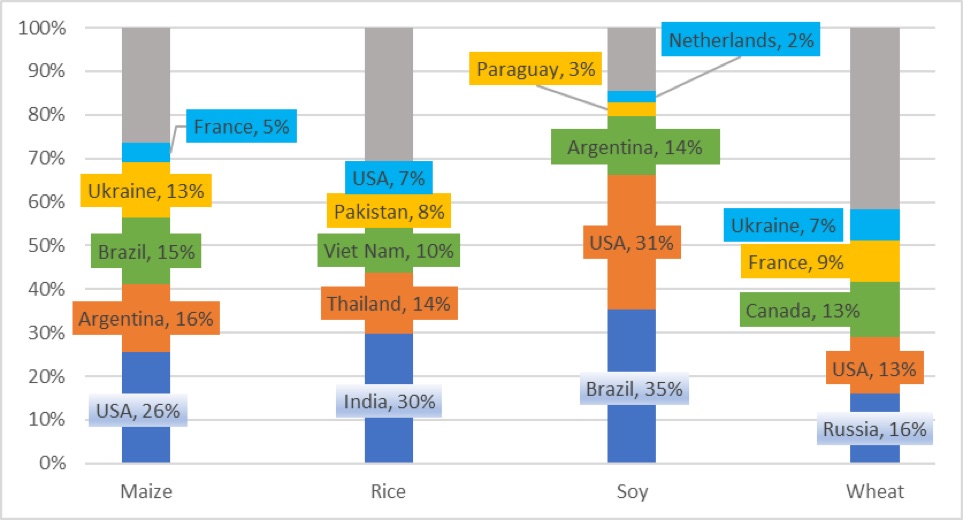

‘Friend-shoring’, however, is not always easy given the fact that a number of soft commodities can only be produced economically and in sufficient quantities in a few countries and substituting these products with alternatives is often difficult. Figure 3 illustrates the extent of this concentration for maize, rice, soy and wheat where the top five producing countries account for between 58% and 85% of the global exports for these commodities.

Figure 3: Top five producers (percentage of 2020 global exports in USD, FAO data, Planet tracker analysis)10

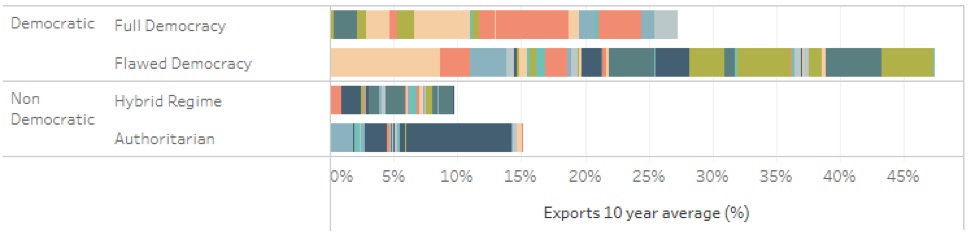

In spite of this concentration of suppliers for some commodities, the supply chain risk of export restrictions is reduced by the fact that only 25% of ‘renewable nature-dependant exports’ (NDE) were supplied by ‘non-democratic’ regimes as discussed in our blog, The Politics of Nature Dependent Trade – see Figure 4.11

Figure 4: Renewable nature dependant exports value totalled $2.4trn 2010-19 with 25% from non-democratic states12

While the wide variety of democratic and non-democratic regimes involved in soft commodity production suggests that geopolitical pressures are less likely to cause a rapid decoupling in the global food system than has been the case with energy (for example), the geopolitical pressures exist nonetheless and add weight to the argument for reducing supply chain risk and complexity.

Would shorter food supply chains benefit the planet?

Commentators (and restaurants) often talk about ‘food miles’, the climate impact of transporting food, and academics estimate that that transport is responsible for nearly 5% of the food system’s total emissions,13 so shortening supply chains would seem to be a desirable outcome, particularly in relation to fruit and vegetables, where refrigerated transport adds to the carbon footprint. However, it’s important to distinguish between shorter food supply chains and more sustainable food supply chains since they are not necessarily the same. For example, it might be technically possible to produce soy in Norway for the Norwegian market using large amounts of energy, but the carbon footprint overall would be higher than growing soy somewhere like Brazil or the USA where the energy required is much lower (and more than offsets the impact of transporting the soy to Norway).

In its 2019 report ‘Growing Better: Ten Critical Transitions to Transform Food and Land Use’ the Food and Land Use Coalition (FOLU) included a recommendation to build ‘local loops and linkages’ as a way to reduce food waste and create jobs.14 If these ‘local loops’ are supported by regenerative agriculture and a more diversified crop base (as recommended by FOLU) the result would be even more beneficial from a planetary perspective.

We do not expect the invasion of Ukraine to lead to rapid decoupling of food system supply chains more generally because the effects are restricted to specific commodities. But the food price crisis that has resulted is another reason for companies and governments to focus on where they source their food supplies.

Shortening food supply chains in a sustainable manner can have the mutually beneficial impacts of increasing food security whilst reducing the food systems environmental footprint. It would also have the benefits of providing more control and transparency, both critical in managing the high inflation currently within the food system and essential for building a more sustainable food system that supports internationally agreed climate and nature goals.

On that basis, the current food crisis sparked by the invasion of Ukraine might provide helpful impetus towards the required transformation of the food system.

2 https://home.treasury.gov/news/press-releases/jy0714

3 https://www.bain.com/insights/us-china-decoupling-tech-report-2021/

7 https://www.sciencedirect.com/science/article/pii/S2211467X2030064X

10 FAOSTAT https://www.fao.org/faostat/en/#data/TCL