Single-Use Plastic: Accounting for Change

Just as sustainability standard setters are consolidating into the more powerful International Sustainability Standards Board (ISSB), an influential participant, the Sustainability Accounting Standards Board (SASB), has recommended improved disclosures for plastics risks and opportunities. It warns of rising scrutiny from regulators, consumers, and companies driven by environmental externalities primarily associated with single-use plastic production and disposal. Also, it highlights the significant financial implications for companies in the chemicals/plastics industry and, in turn, its investors. Asset owners and managers should be supporting the implementation of these proposals as soon as possible.

Standard setters consolidate

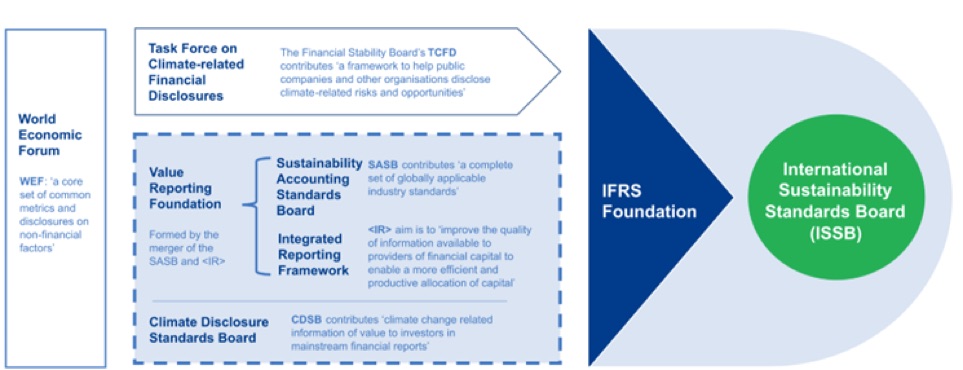

At the end of this month, the Value Reporting Foundation1 – home to the Integrated Thinking Principles, Integrated Reporting Framework and the SASB Standards – will consolidate under the IFRS Foundation,2 which is establishing the new International Sustainability Standards Board (ISSB). The ISSB has announced its intention of ‘building upon the SASB Standards and for embedding SASB’s industry-based standards development approach into the ISSB’s standards development process’.3

In addition to the Value Reporting Framework, the ISSB has also pledged to work with other existing investor-focused reporting initiatives including the Climate Disclosure Standards Board (CDSB), the Task Force for Climate-related Financial Disclosures (TCFD), and the World Economic Forum’s Stakeholder Capitalism Metrics. This will clear the way for the ISSB to become the global standard-setter for sustainability disclosures for the financial markets4 – see Figure 1.

Figure 1: Shaping Sustainability Disclosure Standards (relation between SASB and ISSB) / Source: KPMG5

Prior to this imminent merging of sustainability standard setters, the Sustainability Accounting Standards Board (“SASB”) has highlighted the growing risk associated with single-use plastics (SUP) and proposed that corporates provide greater transparency on these risks and opportunities. See “Plastics Risks and Opportunities in the Chemicals Industry”.6 Note that SUP is defined as products that are made wholly or partly from plastics and are typically intended to be used just once, for a short period of time, before disposal.

Reasons behind the recommendations

SASB highlights a large number of reasons to improve the transparency associated with the management of SUP, including:

- Increasing scrutiny from regulators, consumers, and companies

- Environmental externalities primarily associated with production and disposal

- Low recovery rates and challenges in recycling (including inadequate recycling facilities capacity leading to waste often being discarded to landfills and oceans)

- Export restrictions and waste import bans (e.g. Chinese Operation National Sword7)

- Increasing risks to company brands from viral images of marine animals that have inadvertently consumed plastics

- Product bans (e.g. straws, cotton buds, plastic cutlery etc.)

- Requirements to incorporate alternative raw materials

- Possible taxes and fees in some jurisdictions

The financial risks to the chemicals industry cited by SASB were: “revenue risks and opportunities associated with shifting demand toward alternative products, increased investments in research and development (R&D) and capital expenditures for developing alternative products, and possible costs associated with changing regulations.” An example of revenue risk is provided by the Minderoo Foundation’s research paper – The Plastic Waste Makers Index – which highlighted that the top 20 resin producers generate more than half the global single-use plastics waste.8

Regulatory issues were also high up the agenda with more policies relevant to SUP impacting all plastics value-chain players, adding extra financial stress in the industry, and possibly leading to costs (fees, fines etc.) and a reduced end-market. But the SASB paper quite correctly, not only comments on regulatory risks, but also opportunities, ‘The shifting regulatory and demand landscapes for traditional plastic resins, polymers, and alternatives are increasingly likely to present revenue risks and opportunities for companies in the chemicals industry’.

It is difficult for investors to ignore these headwinds and some are responding. ‘A growing body of investment research and products related specifically to the issue of plastics and plastic waste’ is observed in the investor feedback to SASB, as is the launch of some ‘plastics-focused investment products’. SASB ‘identified significant evidence of investor interest regarding single-use plastics management’. Planet Tracker notes this rising interest but cautions that this is from a very low level. In ‘ESG Proposals: Will Investors Support Them?’ Planet Tracker observed that over the last five years that plastic has only been raised 8 times at annual shareholder meetings, although we recognise that this excludes pre-meeting agreed policies resulting in the proxy being withdrawn. In addition, we view international negotiations on plastic pollution as a positive step, but also note the lack of support from some financial institutions and corporates. See ‘Hiding Away’

Key recommended changes

SASB proposes five new metrics to the ISSB. These appear both reasonable and undemanding for corporates to implement. Investors should require these from corporates as soon as possible.

- Revenue from products sold for use in the manufacture of single-use plastic. This would provide an insight on the extent to which a company’s revenue may be at risk. There was pushback, with some chemical companies proposing a range, rather than a single point, and volumes rather than price information. Some chemical companies pointed out that they are not the direct manufacturer of single-use plastics or end-products, and the polymers they produce can be used for various plastic products, therefore an accurate figure may be difficult to provide.

- Revenue associated with products that intend to reduce the environmental impacts associated with single-use plastics throughout the product lifecycle. This would provide investors with data on a company’s ability to capitalize on potential opportunities, for example.

- Expenditures: (1) R&D expenditures and (2) capital expenditures associated with business activities that intend to reduce environmental impacts associated with single-use plastics throughout the product lifecycle. This would be a valuable input when assessing a corporate’s strategy and commitment to these new business areas. Note that for points 1, 2 and 3, that some corporates argued that providing percentages was more cost effective, but investors prefer the absolute amount as there is less room for ‘inconsistent compilation’.

- Percentage of total raw materials processed for use in the manufacture of inputs for single-use plastics products, by (1) virgin fossil fuel (hydrocarbon) content, (2) recycled content, and (3) renewable materials. This would provide valuable information on company’s capability in relation to existing or upcoming regulations as well exposure to changing demand for SUP products.

- Discussion of actual and potential environmental and social impacts from business activities intended to reduce the environmental impact of single-use plastics occurring. This allows investors to assess various alternatives to single-use plastics products based on a concern that there could be unintended consequences, such as environmental and social impact trade-offs from some alternative solutions. An example of this would be changes in food packaging causing greater food waste.

Looking forward

The risks and opportunities related to the existing plastic business model are coming under increasing scrutiny – see ‘Breaking the Mould’. We are delighted that SASB is putting forward proposals to aid this scrutiny. These proposals are simple changes and if supported by the ISSB, would provide investors with valuable information about their SUP exposure, allowing them to more accurately determine the risks and rewards for themselves. But rather than waiting for the ISSB to change its rules, investors should demand this information now.

1 Value Reporting Foundation

2 International Foundation Reporting Standards (IFRS) Foundation is a not-for-profit, public interest organisation established to develop a single set of high-quality, understandable, enforceable and globally accepted accounting and sustainability disclosure standards—IFRS Standards—and to promote and facilitate adoption of the standards. These standards are developed by our two standard-setting boards: the International Accounting Standards Board (IASB) and the newly created International Sustainability Standards Board (ISSB). The IASB sets IFRS Accounting Standards and the ISSB sets IFRS Sustainability Disclosure Standards.

3 IFRS News 31 March 2022

4 ISSB: Frequently Asked Questions

5 A new standard setter for sustainability reporting – KPMG Global

6 https://www.sasb.org/standards/process/active-projects/plastics-risks-and-opportunities-in-chemicals-industry/

7 PR Newswire – China’s National Sword Policy

8 The Plastic Waste Makers Index – The Minderoo Foundation