Out of Sight – but not Out of Min(e)d

Supporters of deep-sea mining promise to provide the materials needed for a decarbonised future by extracting key metals from the seabed. However, the environmental effects of deep-sea mining have shown catastrophic and irreversible implications for biodiversity. Nauru, the Micronesian island, has recently notified the International Seabed Authority (ISA) that its sponsored entity, Nauru Ocean Resources Inc. (NORI), plans to commence deep-sea mining in two years’ time. In turn, this triggered a rule embedded in the U.N. Convention on the Law of the Sea (UNCLOS) to create deep-sea mining regulations, or to evaluate the proposal directly. Only Nation States can apply to the UN for rights to mine. Therefore, Canadian-based The Metals Company (TMC), has created a company in Nauru to front its application to mine. However, TMC is facing financial problems as investors pull out over claims of financial misrepresentation and environmental risks. And companies such as Google, BMW and Samsung SDI have stated they will not purchase materials from the deep sea. Is deep-sea mining dead in the water? We fear not.

What is Deep-Sea Mining?

The deep sea is defined as areas at a depth greater than 200m, covers around 50% of the Earth’s surface (∼360 million km2) and represents 95% of the space in which organisms can live.1 Deep-sea mining is the process of retrieving mineral deposits from the seabed, notably copper, cobalt, zinc, manganese, silver, gold, lithium, and nickel. Deep-sea mining mainly refers to three activities:2

- Cobalt-Rich Crusts (CRCs) at Seamounts: Mining CRCs which form on the slopes and summits of seamounts at a depth of 800-2,500 meters below the surface.

- Seafloor Massive Sulphides (SMS) at Hydrothermal Vents: Excavating active and inactive geothermal vents at a depth of 1,000-4,000 meters below the surface.

- Polymetallic Nodule Collection: The collection of potato-shaped manganese and iron nodules 4-10cm in diameter between 4,000-8,000 meters below the surface, found on the abyssal plane.

Mining in shallow waters already takes place. For example, Diamond Fields International’s Namibia operation has been extracting diamonds since 2001. However, no commercial-scale mining operations currently take place in the deep sea.4

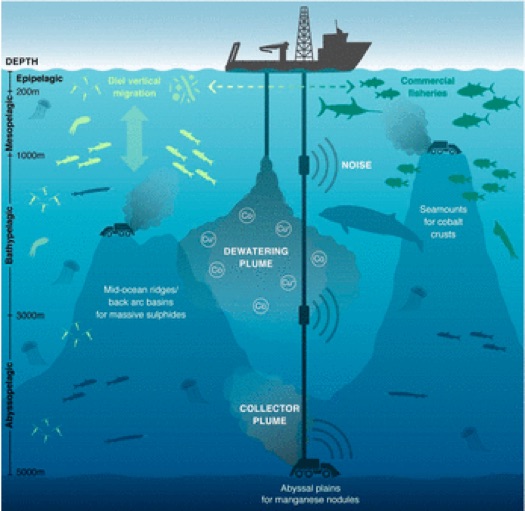

The current experimental contracts for the extraction of seabed materials use a seafloor collector vehicle to mine mineral rich crusts or collect nodules, a transport system to carry the ore and sediments to a surface vessel, shipboard system to separate ore-bearing materials (known as dewatering), and a pipe to discharge waste sediments and water back into the sea – see Figure 1.5

Figure 1: Deep-sea mining diagram.3

Ecological Impact of Deep-Sea Mining

Some argue that deep-sea mining is a more environmentally sensitive way to extract minerals. Canadian based The Metals Company (TMC) states on its website the green credentials of deep-sea mining, producing 0% solid processing waste and 1% toxicity relative to conventional land-based mining.6 However, this is widely disputed and when viewed from a supply chain perspective, once collected the metals must be processed on land, creating waste. In addition:

- Long term experiments suggest catastrophic, irreversible damage to seabed communities. Areas which had been subject to simulated deep-sea mining, such as the DISCOL project – a DIS-turbance and re-COL-onisation experiment in a Manganese Nodule Area in the Southeast Pacific Ocean off of Peru, funded by the former Ministry of Science Technology of the Federal Republic of Germany from 1988 to 1997 and the first large-scale experiment of its kind investigating nodule collection in deep sea environments, still showed significant ecological impacts after 26 years.8

- Evidence suggests that microbial activity in or near areas of mining were reduced fourfold. Recovery is shown to be slow. Microbial cell numbers were reduced by ~50% in fresh mining plough tracks9 and by <30% in the old tracks. Growth estimates suggest that microbially mediated biogeochemical functions need over 50 years to return to undisturbed levels.10

- Release of slurry from waste pipes will have both acute and diffuse impacts. Previous experiments involving Deep-Sea Tailings Placement (DTSP) – where terrestrial mining waste is released into the deep sea – demonstrate chronic reductions in biodiversity and biomass for decades after release and across sampled depth ranges, covering at least 1,000m of the water column.11 Waste discharged higher in the water column can travel further distances.

- Concern grows on the disruptive effect that mining could have on existing or threatened fish population biomass, ecosystem connection (between shallow and deep seas), carbon sequestration, nutrient regeneration, and provision of harvestable fish stocks.12

Prospected areas such as the Clarion-Clipperton Zone (CCZ), a 4.5 million square kilometre zone in the north-eastern equatorial Pacific, are also home to many endemic species not found anywhere else. Due to the nature of low nutrient and energy deep sea environments, ecological recovery from mining is projected to take decades – see infographic.

Why Mine the Deep Sea?

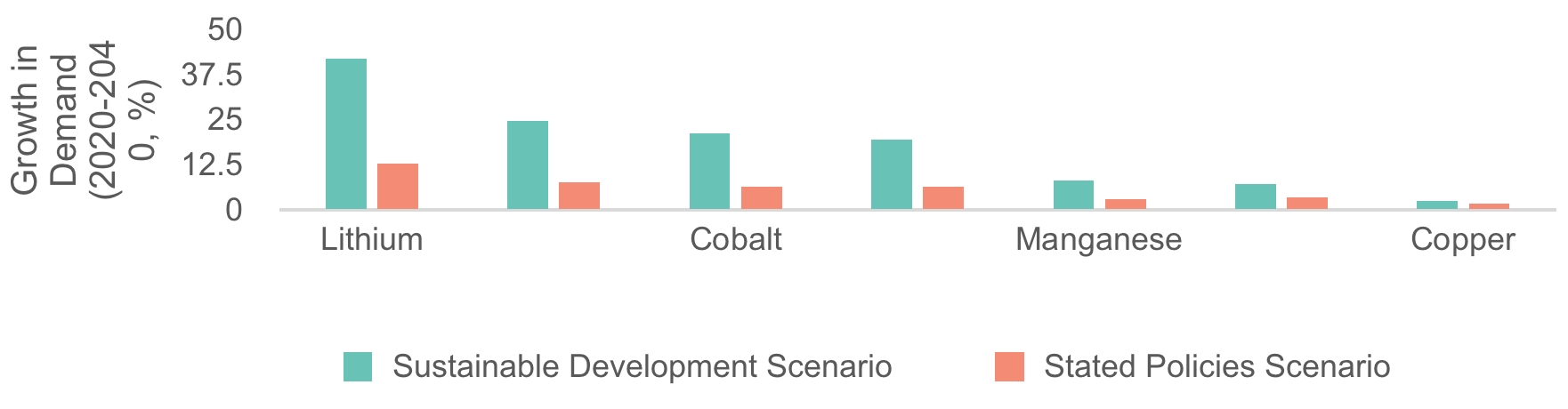

Under the transition scenario to sustainable energy sources, demand for precious metals (i.e., lithium, nickel, cobalt, manganese, and graphite) will boom, as those materials are crucial to battery performance, longevity, and energy density. Figure 2 projects the demand for minerals to 2040 under business-as-usual (stated policies) and transition (sustainable development) scenarios.13 For the transition to low or net-zero carbon emissions to be meaningful, procurement of the key minerals below must be done in a manner which does not exacerbate the earth’s ability to regulate carbon and nutrients at scale (whether land or ocean), otherwise the harmful projections of physical risk and ecological decline under warming climates will be felt despite the shift towards electrification.

Figure 2: Projected change in demand for precious metals under business-as-usual and transition scenarios, 2040 relative to 202014

The Environmental Case for Deep-Sea Mining is Weak

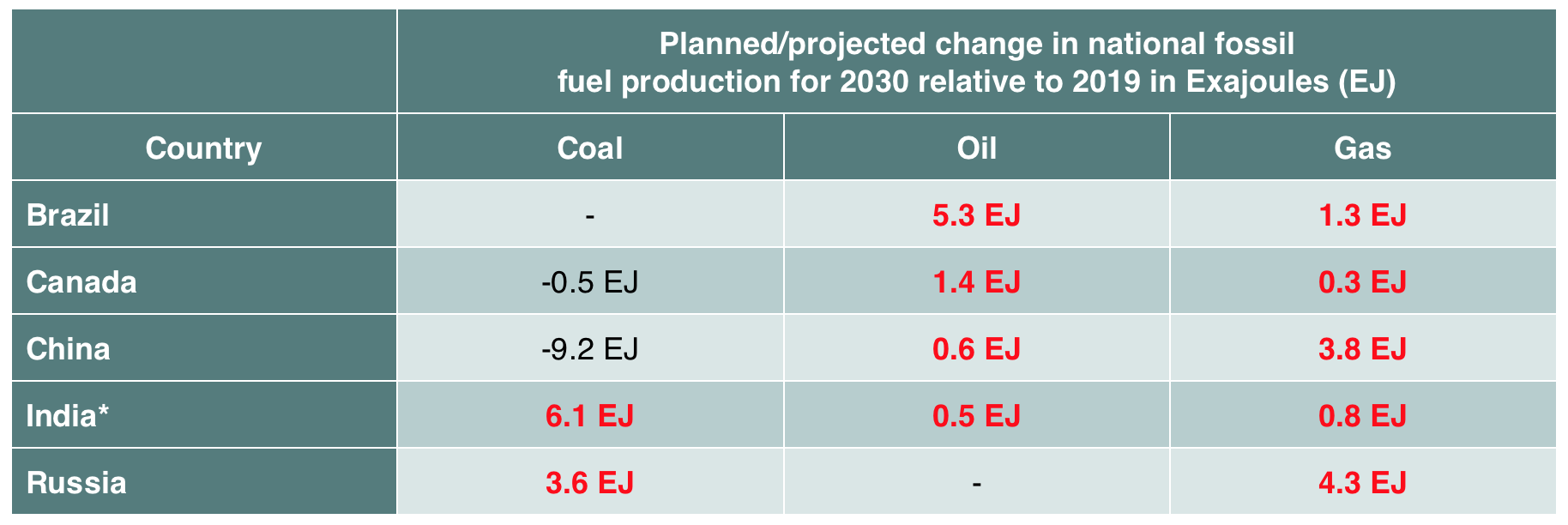

Many countries which support deep-sea mining developments are also lagging behind on climate commitments. Analysis in 2021 demonstrated that governments plan to produce more than twice the amount of fossil fuels in 2030 that would be consistent with limiting warming to 1.5ºC, with many producers planning to continue or increase production.

As shown in Table 1, domestic energy consumption measured in exajoules, is expected to increase to 2030. Specifically, these expansion plans would breach climate tipping points, with 240% more coal, 57% more oil, and 71% more gas than would be consistent with limiting global warming to 1.5°C under the current trajectory.16

Table 1: Planned Change in National Fossil Fuel Production 2019-2030. *For India, changes shown are for 2024 relative to 2019

Unless governments which back seabed mining also embrace a sustainable energy transition, the environmental arguments to the upside of deep-sea mining hold little credibility. Without efficient and holistic use of resources – not just material exploitation, but recycling and robust climate commitments – the need for these materials as crucial elements for slowing catastrophic climate change becomes more doubtful. Will the global community get the worst of both deals: runaway climate change and ecological destruction?

Where is Deep-Sea Mining Due to Take Place?

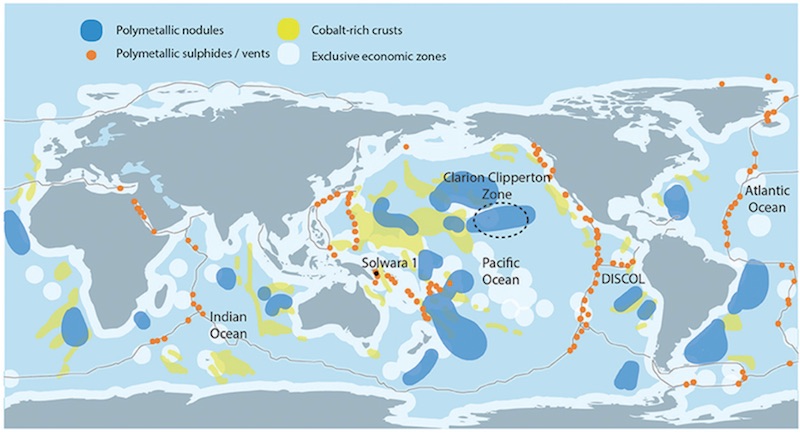

The focus for mining of polymetallic nodules is mainly in the Clarion Clipperton Zone (CCZ), comprising 55% of current outstanding exploration contracts, as well as in the exclusive economic zones (EEZs) of several nations – see Figure 3.18

Figure 3: A 2013 world map showing the location of the three main marine mineral deposits: polymetallic nodules (blue); polymetallic or seafloor massive sulphides (orange); and cobalt-rich ferromanganese crusts (yellow).19

The regulatory regime

The deep-sea mining regulatory regime is administered by the International Seabed Authority (ISA), an autonomous organisation within the United Nations, headquartered in Kingston, Jamaica. It was established through a mandate of the United Nations Convention on the Law of the Sea (UNCLOS) with the responsibility of regulating exploration and exploitation of oceanic minerals.20 Currently, 167 countries and the European Union are Members States21, while 3022 are participating as ISA observers.

While the ISA has developed regulations to govern exploration, it is now focused on developing a regulatory regime for resource exploitation. In the ISA Strategy Plan (2019-2023), one of the key issues deals with provisions relating to environmental protection. The main focus of discussions will concern measuring environmental impact and set boundaries of deep-sea mining (i.e., draft guidelines for the establishment of baseline environmental data and impact assessment process as well as the draft guidelines for the preparation of environmental management and monitoring plans).23 For a timeline of ISA 27th Session meetings, see Table 2.

Table 2: ISA 2022 meetings concerning the draft regulations on exploitation of mineral resources in the deep sea.24

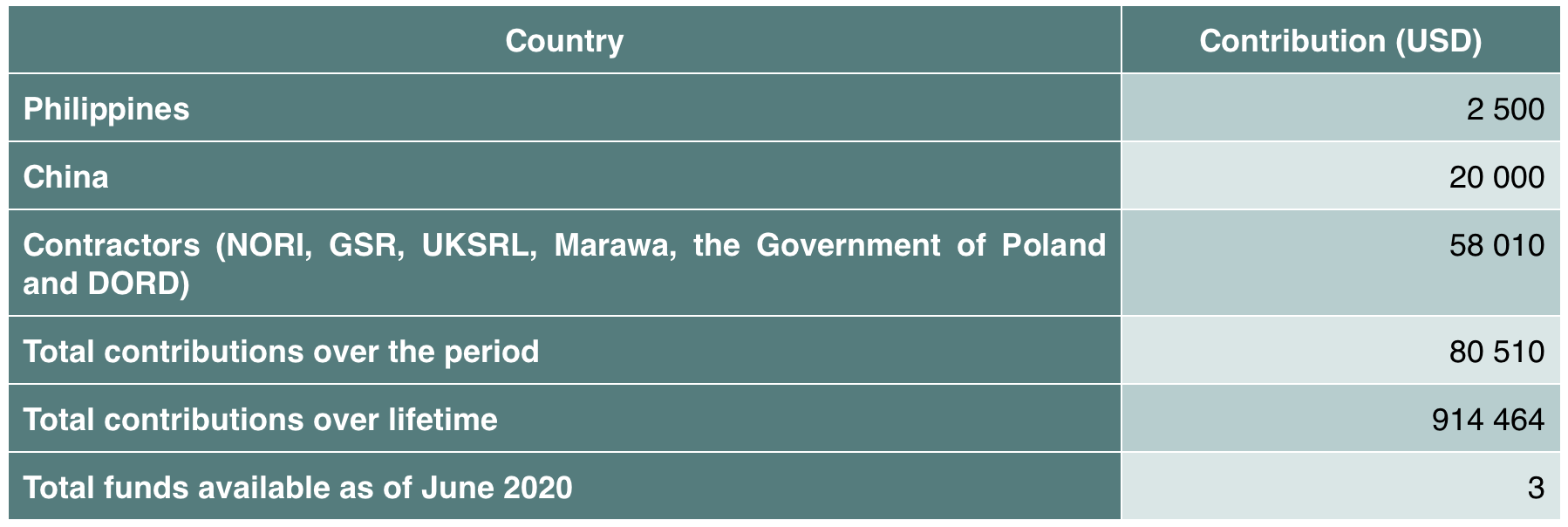

As stated in the ISA’s 2020 Annual Report “Until ISA has sufficient funds from other sources (e.g., royalties from deep-sea mining) to meet its administrative expenses, those expenses shall be met by assessed contributions of its members”.25 Note the references to royalties.

It is also significant that some of the trust and voluntary funds are also used to finance the ISA. For example, the trust fund for the Legal and Technical Commission and the Finance Committee received 72% of its contributions from mining contractors – see Table 3.

Table 3: Voluntary trust fund for the members of the Legal and Technical Commission and the Finance Committee Contributions – July 2019/June 2020.26

Developed Countries Sponsor Corporates to Mine the Pacific or Indian Oceans

Deep-sea mining ventures are highly capital intensive. In 2011, it was estimated that a total investment of USD 1.95 billion as capital expenditure and USD 9 billion as operating expenditure was needed for a single deep-sea mining venture (typical area of 75,000 km2 with an estimated nodule resource of more than 200 million tonnes).

These costs would rise if regulatory or civil society action slow or restrict mining from taking place once the assets have been purchased.27

Such an investment would yield about 54 million tonnes of metals with a gross in-place28 value of USD 21–42 billion over a mine site’s 20-year life span, meaning expected returns are high.

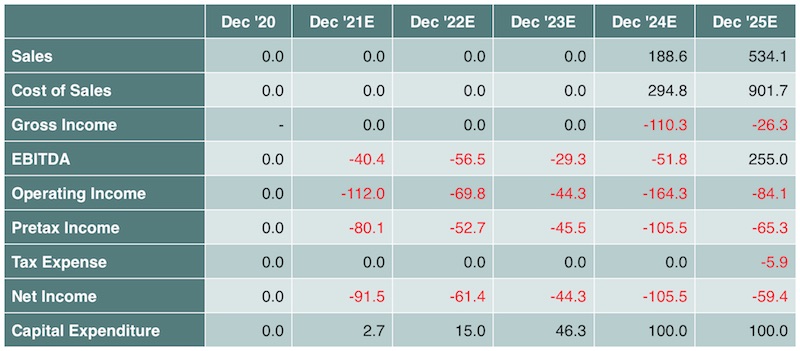

For instance, TMC is forecast to achieve an EBITDA margin of 48% in 202529 – see Table 4.

Table 4: Estimated Financial Performance, The Metals Company, 2020-2025. All currency in USD Million.30

Alongside high initial capital expenditure requirements, under the United Nations Convention on the Law of the Sea (UNCLOS), private mining companies must be sponsored by a state in order to mine the seabed.31

The Pacific island nation of Nauru has stated its intention to start commercial deep-sea mining in two years’ time, through Nauru Ocean Resources Inc (NORI), despite the fact that the International Seabed Authority (ISA) has yet to agree upon overarching rules and regulations.32

By invoking a “two-year” rule in UNCLOS, the ISA must adopt rules, regulations, and procedures to govern the proposed mining activity and if these negotiations do not complete by the end of the time period, the regulatory body must evaluate the mining proposal regardless.

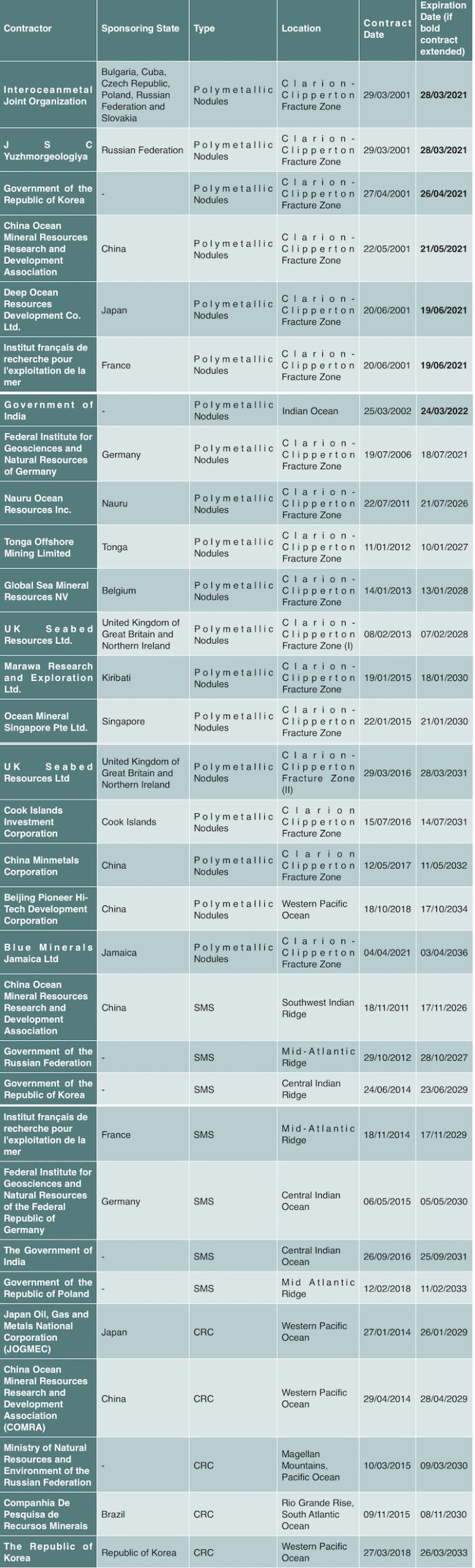

NORI is not alone in wanting to explore and extract from the seabed: the ISA has entered into 15-year contracts for exploration for polymetallic nodules, polymetallic sulphides and cobalt-rich ferromanganese crusts in the deep seabed with 31 contractors, mostly within the CCZ and sponsored by developed countries such as China, Germany or France – see Table 5.33

Table 5: A summary of mineral exploration contracts in the Area approved by the ISA *All contract holders must either be owned by a government or sponsored by a government. Clarion Clipperton Zones (CCZ) of the Pacific Ocean; seafloor massive sulphide deposits, (SMS); cobalt rich crusts (CRC). Source: International Seabed Authority.34 **Contract expiration date extended if in bold.

The Financial Lessons to Date

Companies have attempted to commence deep-sea mining before, but were hampered by technological, regulatory, and civil society action. For example, in April 2021, halfway through the Belgian firm GSR’s programme of trials, a 25-tonne mining machine detached from the surface ship and was stranded on the seabed, demonstrating the additional capital required to overcome technological hurdles which still exist.35

Notably, in 2019, Canadian underwater mineral exploration firm Nautilus Minerals filed for bankruptcy after attempting to restructure but failing to find a buyer for any of its assets.36 Similar to Nauru and NORI, the Papua New Guinea government had invested in Nautilus’ venture – owning a 15% stake in their Solwara I project and equipment. Following the project’s failure, they were left facing USD 24 million in debt – about 10% of their international currency reserves.37,38

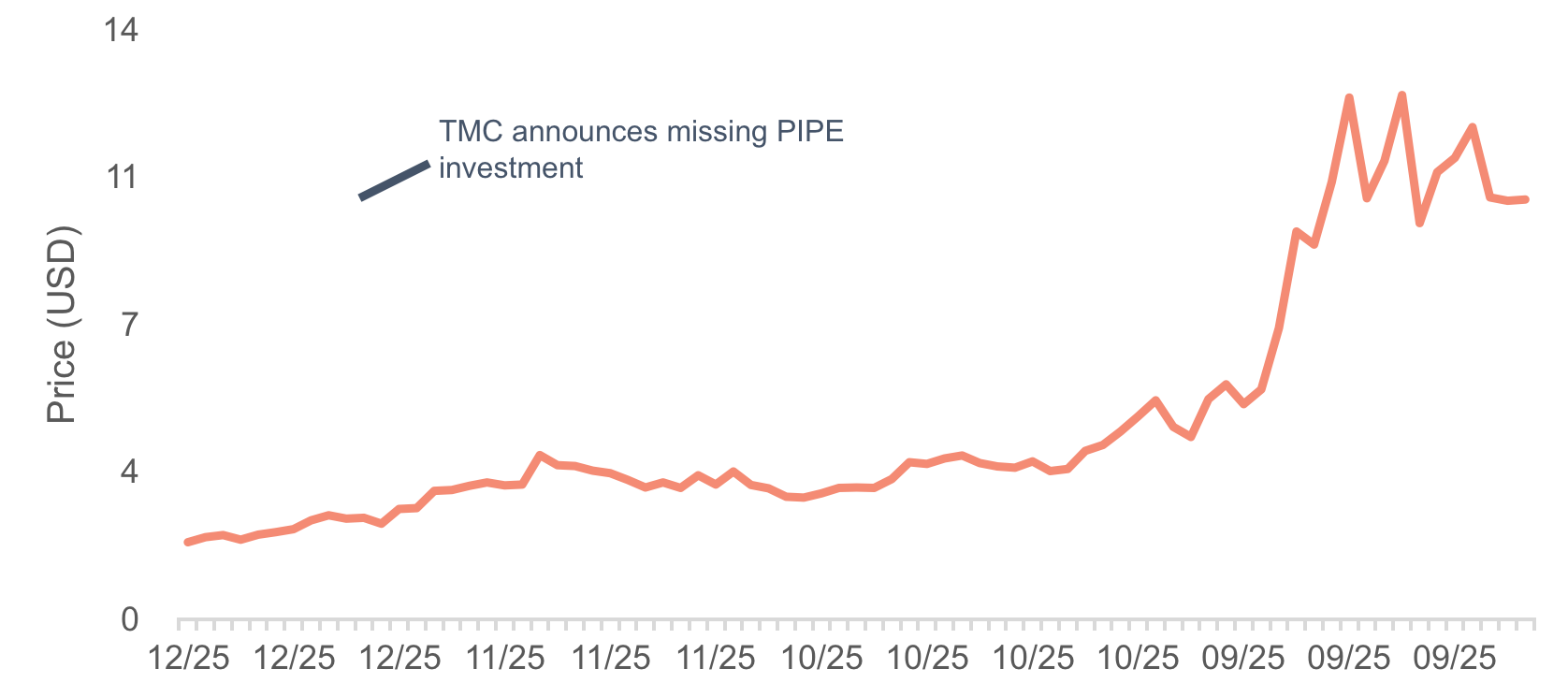

This story could be repeated by Canadian mining company The Metals Company (TMC) which, in Q4 2021, brought the financial risks associated with deep-sea mining to the forefront.

- TMC publicly listed following the merger with the Special Purpose Acquisition Vehicle (SPAC) Sustainable Opportunities Acquisition Corporation and began trading on the NASDAQ on 10th September 2021.39

- By the end of September 2021, The Metals Company (TMC) disclosed two major Private Investments in Public Equity (PIPE) had withdrawn their investments – leaving USD 200 million hole in the company’s books.40

- This in turn led to a 70% drop in share price – see Figure 4.

- Following the share price drop, 90% of TMC’s investors redeemed their shares rather than invest, leaving less than USD 30 million in the SPAC trust.41

- TMC ultimately succeeded in raising only USD 137 million – far shy of the estimated USD 7 billion needed to begin large-scale production.43

Figure 4: The Metals Company’s share price, October 2020 – October 2021 (USD).44

To make matters worse for TMC, in the same month as their cash flow and value significantly dropped, the IUCN Congress voted overwhelmingly in favour of a moratorium on deep-sea mining, although this contains no binding resolutions, it sets the scene for an extended and antagonistic relationship between mining companies and international groups. 45

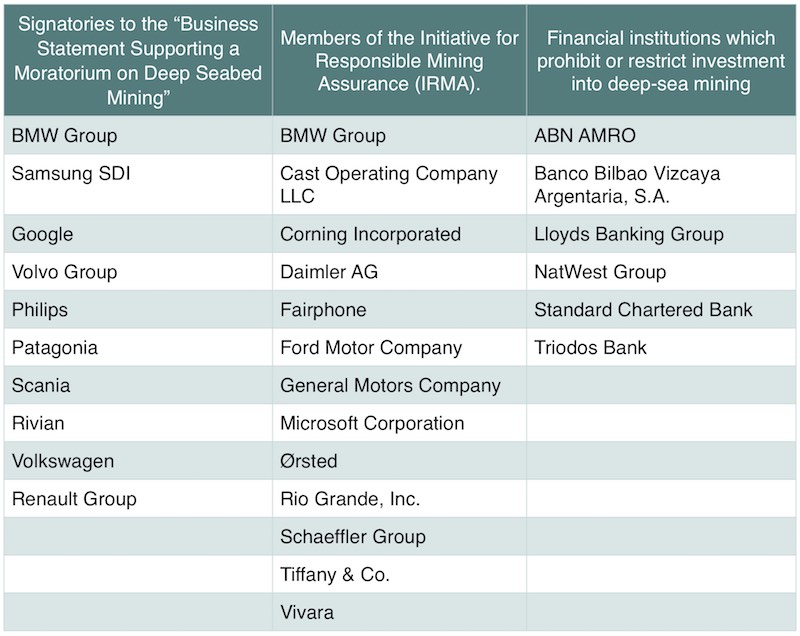

Unstable cash flow from unsure investors, combined with the promise of a regulatory battle to begin operations in earnest, has undermined much of the existing investor and corporate confidence – compounded by companies such as Google, BMW, AB Volvo Group and Samsung SDI stating they will not purchase materials from deep-sea mines.46 For a fuller list of corporates, please see Table 6. Planet Tracker encourages more corporates to exclude deep sea mining from their supply chains.

Table 6: Corporates who have signed the Deep Seabed Mining Moratorium, Corporates who do not allow deep-sea mining products in their sourcing (as per IRMA guidelines), and financial institutions positioned against deep-sea mining.47

Conclusion: Not so Promising

Deep-sea mining has distinct impacts for investors, companies, Small Island Developing States (SIDS), and the environment:

Investors, companies, and SIDS:

- Regulatory pressure could delay the start of deep-sea mining contracts, especially if the ISA implement science-based policy and regulations.

- Delays would increase operational expenditure on existing contracts and may cause more companies to collapse.

- Historically, this has left developing SIDS out of pocket, these contracts potentially being more predatory than productive for SIDS, further jeopardising their ability to adapt to and mitigate climate change-related threats.

Environment:

- Despite its potential role in increasing the availability of battery materials, the ecological damage caused by deep-sea mining may irreversibly affect the ocean’s ability to cycle nutrients and store carbon, weakening the buffers of runaway climate change.

Whilst forecasted returns from deep-sea mining may appear attractive, recent experiences raise questions about their robustness. Given the enormous damaging potential that this industry could have on ocean ecosystems, it is vitally important that a financial case against ocean mining is made in order to prevent the industry from ever getting started. The world does not know much about deep-sea mining but what we do know now should incentivise us from stopping its development.

However, the creation of a regulatory framework for deep-sea mining alongside improving technology and a projected internal rate of return (IRR) of up to 25%48 means that companies will continue to attempt to exploit these areas, and that the battle for the deep sea is only just beginning. The upcoming ISA regulations may limit or enable ocean degradation caused by deep-sea mining moving forward.

Investors should be cautious – some have already suffered losses more than once – while the regulator does not have the necessary environmental information to make a reasoned judgment. Due to the large-scale potential of deep-sea mining, the scientific community, civil society and financial markets are obliged to ensure that 95% of the global biosphere in terms of inhabitable volume (i.e. oceans)49 is treated with considerable care. A sustainable alternative to deep-sea mining would be ‘urban mining’, (extraction and purification of precious metals taken from waste streams), which was found to be more cost-effective (and of course also much more sustainable) than virgin mining.50

1 https://www.frontiersin.org/articles/10.3389/fmars.2017.00418/full

2 https://www.frontiersin.org/articles/10.3389/fmars.2017.00418/full

3 https://www.pnas.org/content/117/30/17455

4 https://www.frontiersin.org/articles/10.3389/fmars.2017.00418/full

5 https://www.pnas.org/content/117/30/17455

8 https://www.nature.com/articles/s41598-019-44492-w

9 ‘Tracks’ here refers to the plough tracks left behind following extraction over the top metre of seabed.

10 https://www.science.org/doi/10.1126/sciadv.aaz5922

11 https://www.nature.com/articles/srep09985

12 https://www.pnas.org/content/117/30/17455

15 An exajoule (EJ) is equal to one quintillion (1018) joules

16 https://productiongap.org/wp-content/uploads/2021/10/PGR2021_ExecSummary_web_rev.pdf

17 https://productiongap.org/wp-content/uploads/2021/10/PGR2021_ExecSummary_web_rev.pdf

18 https://miningwatch.ca/sites/default/files/nodule_mining_in_the_pacific_ocean.pdf

19 https://www.frontiersin.org/articles/10.3389/fmars.2017.00418/full

20 https://www.un.org/en/chronicle/article/international-seabed-authority-and-deep-seabed-mining

21 https://isa.org.jm/member-states

22 https://isa.org.jm/index.php/observers

23 https://isa.org.jm/files/2022-02/IWG-ENV-webinar-briefing-note-Feb2022.pdf

24 https://isa.org.jm/sessions/27th-session-2022

25 https://isa.org.jm/files/files/documents/ISA_Annual_Report_2020_ENG_1.pdf

26 https://isa.org.jm/files/files/documents/ISA_Annual_Report_2020_ENG_1.pdf

28 Value of the product before mining costs

29 Mean outlook from 14 investment analysts

30 FactSet (2021).

33 https://www.isa.org.jm/exploration-contracts

34 https://www.isa.org.jm/index.php/exploration-contracts

35 https://www.bbc.co.uk/news/science-environment-56921773

36 https://www.mining.com/nautilus-minerals-officially-sinks-shares-still-trading/

40 https://www.ft.com/content/6675ac1e-a9a0-48d8-b4e9-aee2ef27c7be

41 https://www.ft.com/content/6675ac1e-a9a0-48d8-b4e9-aee2ef27c7be

44 FactSet (2021).

47 http://www.savethehighseas.org/momentum-for-a-moratorium/

48 https://www.mdpi.com/2075-163X/11/2/221/htm