Implementing traceability: seeing through excuses

Supply chain disruptions were front page news in 2021, highlighting an urgent need for companies to be able to track products along their supply chains. Traceability reveals the history, location and application of an item. Management teams sometimes resist implementing traceability systems arguing they are too costly. But are such systems the cost of doing business or a nice to have? Planet Tracker argues they are a necessity and investors should demand their adoption if only for reasons of self-interest – i.e. reducing their exposure to hidden supply chain risks. Now is an ideal time to embed traceability within companies’ supply chains. Below, we explain why.

Traceability allows transparency

Traceability systems allow corporates to track their products from their origin to use, providing identification and measurement. As defined by the ISO, ‘traceability includes not only the principal requirement to be able to physically trace products through the distribution chain, from origin to destination and vice versa, but also to be able to provide information on what they are made of and what has happened to them’.1

Traceability records may be kept in one of the three following ways:

- paper-based – manual paper-based records;

- basic electronic – computerised record-keeping;

- with integrated hardware – using bar codes and readers, RFID tags and scanners.

Integrated hardware is the most reliable type of traceability, especially if the underlying data collection and processing systems are interoperable, meaning that different information technology systems and software applications can communicate and use that information. Blockchain provides one possibility ‘but has not gained much traction yet’. PWC estimate that ‘only 5% of all companies…have implemented blockchain’.2 Traceability provides the data that products meet certain standards or comply with industry regulations such as environmental or employment laws.

All of the above gives management teams the opportunity to share data with stakeholders, providing transparency. In a nutshell, traceability gathers data and knowledge throughout the entire supply chain, while transparency is the act of disclosing this data to stakeholders. For a management team to evidence sustainability claims, it will need a traceability system.

It should be at top of the management’s agenda

Now is an ideal time to embed or upgrade a traceability system within the company’s operations. This should not only be a consideration for corporate management teams but also debt and equity investors and lenders. We outline why:

1. Managing for Risk

Since the onset of the pandemic, supply chain problems have regularly featured in the media. The interconnectivity of global supply chains became starkly obvious when shelves began to empty. High profile stories such as the ‘Ever Given’ container ship blocking the Suez Canal for 6 days3 or the logjam at the two busiest container ports in the US – Los Angeles and Long Beach,4 evidence this. In Europe, there were claims that there was a shortage of up to 400,000 heavy goods vehicle drivers,5 while China was impacted by power shortages, COVID shutdowns at ports and rising commodity prices.6

Also, consumers and governments discovered that industries which were generally unknown to be interconnected started to disrupt deliveries. For example, in the UK, consumers learned of the reliance of ice cream deliveries on natural gas prices and fertiliser plants. As natural gas prices rose, the fertiliser facilities shut down as it became uneconomic – which resulted in CO2, a by-product of the manufacturing process, no longer being available. In turn, this shut off the supply of dry ice – the solid form of CO2 – needed to keep food cold for storage and transport.7

Understanding a product’s inputs and outputs (e.g. waste) as well as its reliance on different forms of transportation, has become an operational necessity. Effective traceability and therefore product transparency allows corporates to anticipate potential disruption and diversify sources. This is simply good risk management.

2. Managing for Sustainability

Recently, a large number of CEOs have made promises on sustainability issues such as lower carbon emissions or outlining a net zero strategy. Commitments from the 2,000 largest companies by revenue can be viewed at netzerotracker. To meet these commitments traceability will be required, especially for scope 3 targets, such as emissions from purchased goods and services or transportation and distribution by companies not directly owned by the reporting corporate.

Planet Tracker has highlighted this issue in the textiles supply chain, for example. Although much of the attention in textiles is focused on fast fashion and the brands we encourage investors and corporates to look further along the supply chain to the often ignored wet processors. The case is simple; a lack of environmental supply chain disclosures prevents investors from properly pricing ESG risks and opportunities.

But traceability will provide ESG data beyond a carbon footprint. It will allow management to analyse other sustainability data – e.g. child labour or deforestation – which can expose both corporates and investors to reputational and/or legal risk. The financial markets are becoming less forgiving when unethical and risky supply chain practices are unearthed.

3. Managing for Profitability

Although corporate management teams may recognise that traceability systems are desirable, they will also need to be convinced that the investment and operational costs provide a suitable return.

Planet Tracker examined this issue of profitability in an analysis of the global seafood processing industry in ‘Traceable Returns’.

The report demonstrated that the typical seafood processor who implements a traceability solution – in this instance being GDST9 compliant – can double their EBIT10 margins.

The driver of this higher profitability results from fewer product recalls, lower product waste and a decline in legal costs, which mainly explain the three-percentage points margin gain. Interestingly, our report showed that it was rarely driven by receiving an environmentally sustainable premium for the seafood product, rather it can create greater market access as some retailers will only permit certified environmentally sustainable products.

Other studies support the link between environmentally sustainable practices and financial performance. Analysis of the fashion industry by Medcalfe & Miralles Miro, demonstrated that ‘there is stronger evidence that better environmentally sustainable practices led to better financial performance and vice versa’.11 A study by researchers at the MIT Sloan School of Management found that consumers may be willing to pay 2% to 10% more for products from companies that provide greater supply chain transparency. Researchers have found that ‘increasing visibility always strengthens consumer trust’ and this gives opportunities ‘for a trust-driven revenue benefit.12

4. Managing for Regulatory Compliance

Corporates may well be forced to adopt traceability in order to comply with new regulations. For example, this is likely to be the case if EU proposals on the regulation on deforestation-free products is enacted.13 The regulation will initially target six commodities most linked to deforestation: coffee, cocoa, cattle, palm oil, soy and wood, as well as derived products. Under the new rules, it will be illegal to sell or export any of the six commodities if they’ve been produced on deforested land converted from January 2021 onwards. Companies, of all sizes, will need information on products sold in the EU to confirm they are deforestation free. The draft is yet to be approved by the EU Parliament and member countries (the EU Commission hopes to achieve this by 2023).

The EU is not alone. The Russian government is considering new regulations making barcoding of seafood products mandatory for traceability purposes – with a particular focus on caviar.14 Other regulations cover such issues as conflict minerals (US Dodd-Frank Act), forced labour (e.g. Australian and UK modern slavery acts, and California Transparency in Supply Chains Act), and food safety (U.S. Food Safety Modernization Act).15 The OECD has examined the trends in environmental supply due diligence and lists identifies 17 legislative developments, polices and related initiatives.16

An economic implementation window

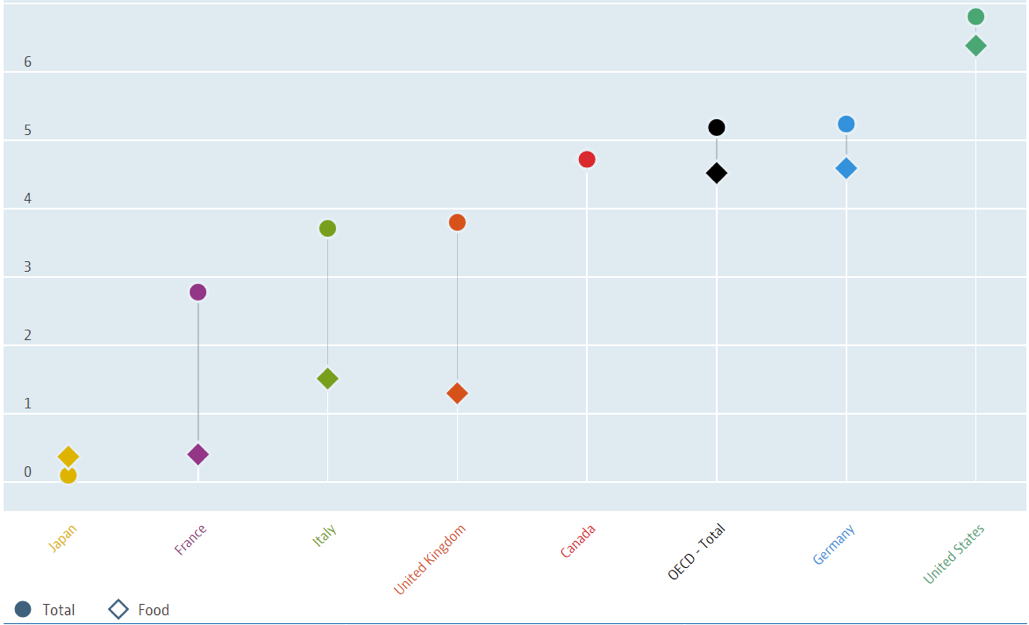

The present economic environment provides an appealing window to integrate a traceability system into a corporate’s infrastructure. Rising inflation, which some central banks believe will be temporary, could provide an excuse for companies to push through price increases in excess of their increased cost base, effectively covering the traceability system’s operating costs. For November 2021, total US monthly CPI data reached 6.8%, while for the OECD it was 5.2% – see Figure 1.

Figure 1: Food and Total Inflation (CPI): Oct 2020-Nov 2021

Source: OECD (2021), Inflation (CPI) (indicator). doi: 10.1787/eee82e6e-en (Accessed on 22 December 2021)

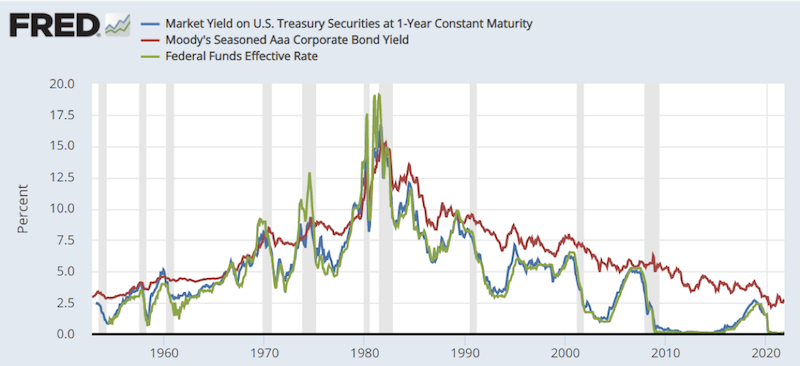

Furthermore, CFOs and Treasurers who have to borrow to fund a traceability system will know that corporate debt rates remain low – see Figure 2. The red line shows the corporate bond yield at 2.6% for November 2021. One further consideration for corporate finance departments is whether they can roll-up improved traceability debt into a sustainability-linked bond (SLB). Planet Tracker has highlighted the increased use of ethical debt in the textile sector and the use of SLBs in the seafood sector.

Figure 2: US Treasury Yield, Moody’s Aaa Corporate Bond Yield & Fund Effective Rate

Source: FRED Economic Data – https://fredblog.stlouisfed.org/2018/04/getting-back-to-normal-part-2/

So why the delay?

One of the major excuses is cost. Expenses will vary considerably depending on the size and complexity of the system required. It is worth pointing out that in some instances there is no cost. Where a large corporate is keen to understand its products’ sources they may require their suppliers to implement such systems and provide an off-the-shelf solution. Recently, Morrisons, the major UK food retailer, has announced the roll-out of a software platform which it is making available to 400 own-brand suppliers, enabling them to improve the accuracy of their greenhouse gas emissions accounting.17 Furthermore, there are organisations that have developed traceability standards and materials – e.g. the Global Dialogue on Seafood Traceability (GDST)18 – at no cost to the user, leaving the corporate to pick up just the IT costs. But even where there is an implementation cost, we encourage management teams to consider the cost savings achievable.

The Food Marketing Institute and the Grocery Manufacturers’ Association has reminded the food industry of the large range of potential costs in addition to direct costs of recalls, which typically include notification (to regulatory bodies, supply chain, consumers), product retrieval (reverse logistics), storage, destruction, unsaleable product and the additional labour costs associated with these activities, as well as the investigation of the root cause. But the most significant costs to the company come from litigation, the costs from any agreed or mandated governmental oversight post incident, lost sales and the impact on the company’s market value and brand reputation.19

If further convincing is required, food recalls in the US have shown a dramatic increase in the last few years, jumping four-fold over the number just 5 years ago. There are multiple reasons for the huge spike in the number of recalls, but a contributing factor includes the increasingly global and complex food supply chain.20

Also high up the list of excuses is the issue of competitive advantage. Transparency can be a worrying topic to many corporates especially as providing a list of a corporate’s suppliers and sources could give away pricing information or other competitive advantages. However, we also wonder whether this obstacle is largely driven by a fear among corporate executives that this information could expose them to criticism. Transparency can empower information users ‘to exert influence on the disclosers and become a tool for holding powerful actors accountable’.21 Is this simply a tussle over the information asymmetry between management teams and their stakeholders – once the latter are in possession of this information they can make more informed decisions?

Planet Tracker are sympathetic with the view of Martinez and Crowther that ‘transparency can be seen to be a part of the process of recognition of responsibility on the part of the organisation for the external effects of its actions and equally part of the process of transferring power to external stakeholders’.22

Returns on investment in supply chain improvements can be very quick. In ‘Uneasy (Un)pickings’ the research demonstrated that for wet processors, which have the largest environmental impact in the textile supply chain, a one-off investment of USD 455K produced an average annual cost saving of USD 369.5K, an average payback period of 13.8 months, an average annualized return on investment of 68%, implying an IRR (internal rate of return) of 33% after two years. Planet Tracker also calculated that implementing a traceability solution typically yields a five-year internal rate of return (IRR) of 39-62% for the average seafood processing company, depending on the implementation costs (5-7% of sales in Planet Tracker’s assumptions). Interestingly, this is above the 39% IRR generated on a typical M&A deal in this industry.23

We have to be realistic that there can be operational obstacles to implementation. Firstly, there can be gaps in the supply chain. For instance, traceability at ‘mixing points’, like processing or modification, can be harder to achieve, resulting in traceability interruptions. As we have mentioned above, large companies are able to ease this problem by making these systems available to suppliers.

There can also be inconsistent industry data standards. This may result from poor data capture and management. For example, the recording of data may be performed manually on paper, which is often inefficient, prone to error, unsecure and forgeable. However, low-cost, user-friendly technologies are abundant, often via a mobile phone, which may alleviate this problem in parts of the world. Where new equipment is required, such as computers, large corporates should consider the case for subsidising these costs as well as providing the necessary training.

Finally, there is sometimes a belief that its benefits are difficult to assess accurately. We dispute this claim and believe that there are numerous benefits as discussed above.

Out of excuses

Investors should demand that companies implement robust traceability systems. If nothing else, investors should do this out of self-interest to ensure they reduce their specific (unsystematic) risk in their investment. But there are other reasons, both financial and ESG or sustainability related. On the former, a reduction in recall or legal costs can underwrite the investment and operating costs but there is also evidence of higher profit margins for those corporates able to certify their sustainability credentials. On the sustainability front, management teams need to ensure they can deliver on their ESG commitments, whether these be their net zero strategy or complying with employment or environmental regulations. When these considerations are mixed with the macroeconomic environment of low corporate debt costs and higher inflation, the case for traceability is compelling.

References

1 https://www.iso.org/obp/ui/#iso:std:iso:12875:ed-1:v1:en

2 https://www.pwc.de/de/strategie-organisation-prozesse-systeme/blockchain-in-logistics.pdf

3 https://www.aljazeera.com/news/2021/7/7/ever-given-ship-which-block-suez-canal-for-months-released

4 https://www.weforum.org/agenda/2021/11/global-supply-chain-crisis-los-angeles-port/

5 https://www.ft.com/content/e8ca2a08-308c-4324-8ed2-d788b074aa6c

6 https://www.globaltimes.cn/page/202110/1236250.shtml

8 Scope 1 covers direct emissions from owned or controlled sources. Scope 2 covers indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by the reporting company. Scope 3 includes all other indirect emissions that occur in a company’s value chain.

9 Global Dialogue on Seafood Traceability (GDST) created standards for seafood traceability Developed by the Global Dialogue on Seafood Traceability (GDST) after three years of discussions convened by WWF and the Global Food Traceability Center at the Institute of Food Technologists, a global research institute based in Chicago, the standards are open-source and non-proprietary, enabling all kinds of companies to use them, from fishers using a mobile phone to large integrated seafood companies.

10 EBIT = earnings before interest and tax

11 Medcalfe, S., & Miralles Miro, E. Sustainable practices and financial performance in fashion firms. Journal of Fashion Marketing and Management. https://doi.org/10.1108/JFMM-10-2020-0217

12 Kraft, Tim and Valdés, León and Zheng, Yanchong, Consumer Trust in Social Responsibility Communications: The Role of Supply Chain Visibility (December 23, 2021) http://dx.doi.org/10.2139/ssrn.3407617/

13 https://ec.europa.eu/environment/publications/proposal-regulation-deforestation-free-products_en

15 https://hbr.org/2019/08/what-supply-chain-transparency-really-means

17 https://www.foodmanufacture.co.uk/Article/2021/12/24/What-is-Morrisons-doing-about-sustainability#

18 https://traceability-dialogue.org/

19 https://www.food-safety.com/articles/2542-recall-the-food-industrys-biggest-threat-to-profitability

20 https://www.food-safety.com/articles/2542-recall-the-food-industrys-biggest-threat-to-profitability

23 https://planet-tracker.org/wp-content/uploads/2021/08/5.-Traceable-Returns.pdf