Ethical debt is the new bespoke fashion

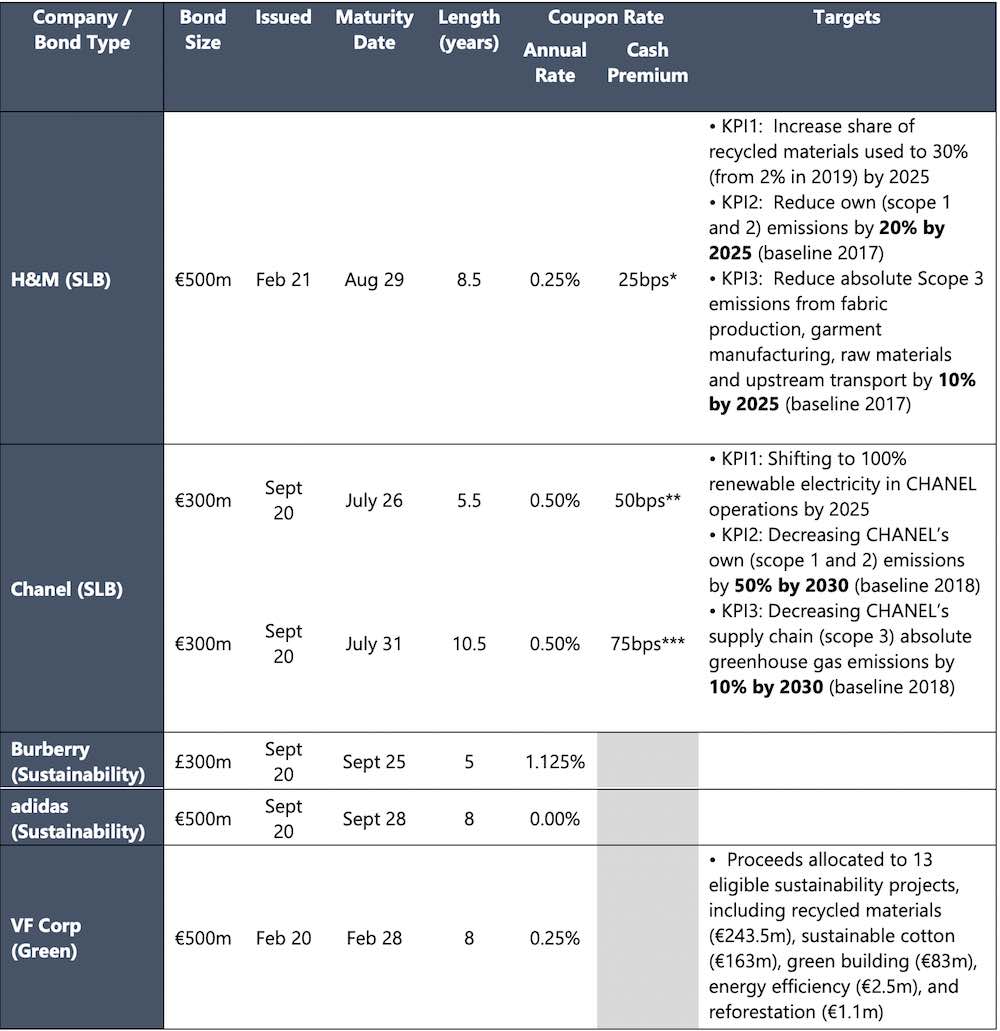

February saw H&M jump on fashion’s latest trend, as they issued a €500m sustainability-linked bond which they will use to meet their 2025 sustainability targets.[i] H&M is the latest in a growing list of apparel companies turning to the ethical and sustainable debt market to fund their sustainability goals. Companies as diverse as Chanel, Burberry and adidas have all raised some kind of green or sustainable debt in the last six months. These bonds are being very well received by the market and have all been oversubscribed.[ii]

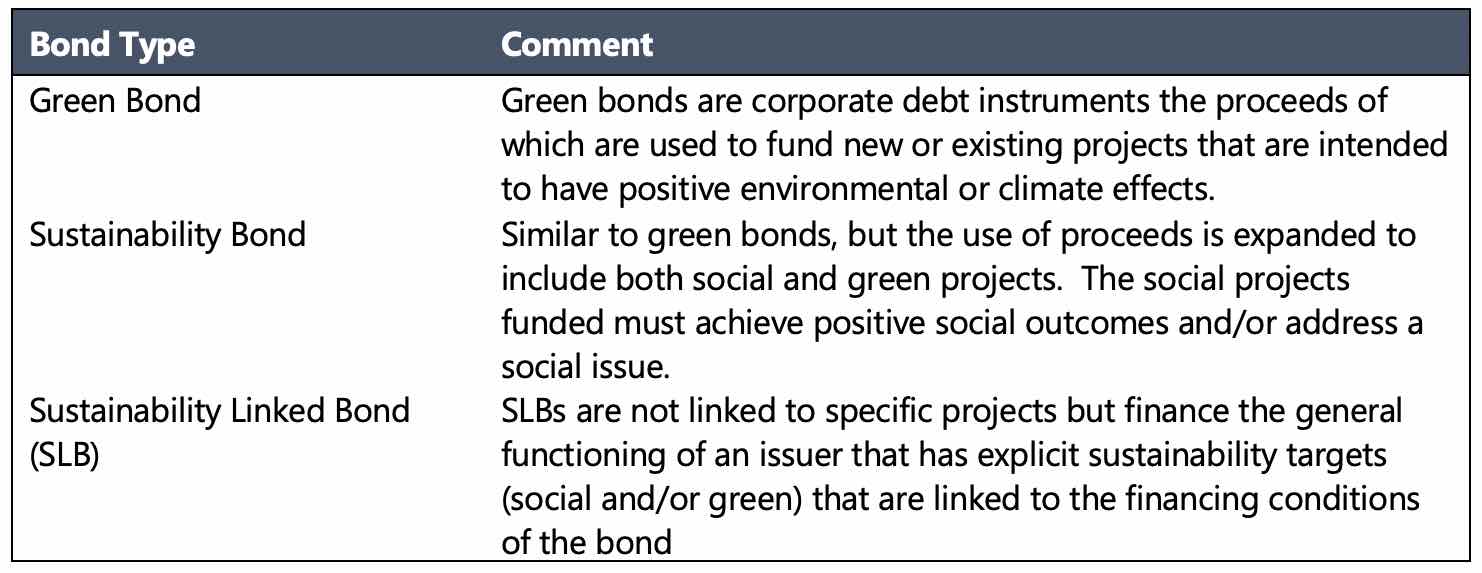

Planet Tracker believes Sustainability Linked Bonds (SLBs) are a positive innovation for the financial markets and for the planet. We believe investors and companies should be embracing these bonds as a positive way to influence change. Unlike straightforward ‘green’ bonds, where the proceeds must be used to fund sustainable (‘green’) projects (see our recent report “Bonds for Ponds”), SLBs are structured with specific measurable and verifiable key performance indicators (KPIs), which if not met, result in the issuing company agreeing to pay financial penalties. Although these “green strings”[iii] must be complied with, the company is not constrained in its use of the proceeds (in line with traditional bonds which are often used to raise capital for ‘general corporate purposes’). To support the development of this market, Sustainability-Linked Bond Principles have been published by the International Capital Markets Association providing guidance around structuring features, disclosure, and reporting, and to allow the bonds to be independently assessed[iv] – see Table 1.

Table 1: Understanding Green, Sustainability and Sustainability Linked Bonds[v]

Divided into two €300m slices (tranches[viii]), the shorter first tranche will pay a cash premium of 50bps on top of the existing rate if Chanel’s first KPI (shifting to 100% renewable energy by 2025) is not met. The second longer dated tranche will pay out an additional cash premium at the end of the bond if the two remaining KPIs are not met. These are emissions-focused and in line with Chanel’s sustainability plans of reducing its own (Scope 1 and 2)[1] emissions by 50% by 2030 and of its supply chain (Scope 3)[2] emissions by 10% by 2030.Chanel and now H&M have been the only apparel companies to utilise these SLBs. Perhaps surprisingly for some, the privately-owned Chanel was the first in the textiles space to do so, announcing their much lauded €600m SLB in September last year.[vi], [vii]

The H&M SLB is structured slightly differently with the final three years of the bond (2026-2029) set to pay out at a higher rate (up to +25bps) depending on if, and then how, any of the 2025 dated KPIs are missed. H&M’s KPIs are also in line with their broader sustainability plans and are arguably more aggressive than Chanel’s. The first is to increase the share of recycled materials used from current levels of 2% to 30% in 2025.[ix] The other two are also emission focused, with the aim of reducing their Scope 1 & 2 emissions by 20% by 2025, and Scope 3 emissions in parts of their supply chain by 10% by 2025 (around 75% of H&M’s total Scope 3 emissions are covered by the KPI in the bond[x] – see Table 2).

Table 2: Sustainable Bonds in the Apparel Industry (Planet Tracker & company reports)

As highlighted by the Quantis report Measuring Fashion, and explored further in the recent Planet Tracker report “Will Fashion Dye Another Day?”, most of the supply chain emissions are due to wet processing. Therefore, for H&M to meet their goals, there will need to be tangible reductions in energy use (and likely water and chemicals use) in the wet processing part of the supply chain which is rarely owned or vertically integrated into he brands. What is particularly noticeable and important about both H&M and Chanel’s SLBs is the focus on reducing emissions in the supply chain. Both have a KPI directly linked to reducing Scope 3 emissions. In the case of H&M, 48% of total reported Scope 3 emissions come from fabric production.vii This is interesting because, as the KPI in H&M’s SLB is just focused on Scope 3 emissions from fabric production, garment manufacturing, raw materials and upstream transport, this means fabric production now accounts for more than 60% of the Scope 3 emissions that H&M are planning on reducing by 10% by 2025.

How H&M and Chanel are planning to target these supply chain emissions is still only briefly outlined. To meet their emissions KPIs, H&M plan to advise their suppliers on how to increase energy savings by creating “a team of engineers fully devoted to reducing energy consumption among H&M Group’s suppliers” and by supporting “our suppliers with financing of emission reduction measures”. We anticipate that to reduce emissions H&M and Chanel will likely need to also invest either directly into their Tier 2 and 3 suppliers, or through other mechanisms such as credit guarantees.

These large brand-based bonds are not the only way debt investors can create change in the supply chain. The Good Fashion Fund (a spin off from Fashion for Good), is an impact fund specifically set up to target long term USD investments in the textile & apparel manufacturers in India, Vietnam and Bangladesh – the key wet processing geographies. The fund specifically finances the implementation of highly impactful and disruptive production technologies, with example technologies such as waterless dying and effluent treatment plants.

We anticipate more SLBs for the apparel industry in 2021 and beyond, as both debt and equity investors look for further ways to tap into the current green trend. SLBs offer accountability of sustainability targets in a more direct way to debt investors, not just equity investors.

But questions do remain. Are SLBs superior to other debt instruments? Could the KPIs be more ambitious? How can we ensure the KPIs are not too generic in nature? We would like to see more bonds split into tranches (portions) with differentiated targets on a variety of timelines for greater accountability. Where should these bonds be focused to drive the biggest impact? If SLBs are more general in nature than their green counterparts, can they be more open to greenwashing? Will meeting or missing KPIs be verified by an independent source? We will watch with interest.

[1] Scope 1 covers direct emissions from owned or controlled sources. Scope 2 covers indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by the reporting company.

[2] Scope 3 includes all other indirect emissions that occur in a company’s value chain.

[i] https://hmgroup.com/wp-content/uploads/2021/02/HM_Sustainability-Linked-Bond-Framework.pdf

[ii] All these bonds have been reported as being oversubscribed in the press. H&M was 7.6x oversubscribed, adidas more than 5x and Chanel just reported as oversubscribed. Clearly the investor appetite for these bond is there.

[iii] https://www.bloomberg.com/opinion/articles/2020-09-17/climate-eu-s-green-bonds-should-come-with-green-strings-attached

[iv] https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/sustainability-linked-bond-principles-slbp/

[v] https://www.pimco.co.uk/en-gb/resources/education/understanding-green-social-and-sustainability-bonds/

[vi] https://www.bloomberg.com/opinion/articles/2020-09-25/fashion-giant-chanel-designs-a-fabulously-fashionable-green-bond

[vii] https://cib.bnpparibas.com/sustain/stitching-luxury-and-science-into-the-sustainability-linked-bond-market_a-3-3754.html

[viii] https://www.investopedia.com/terms/t/tranches.asp

[ix] To provide transparency to investors and in line with the SLBP. H&M “will ensure an external and independent verification by one or more qualified external reviewer(s) with relevant expertise, as outlined in the Voluntary Guidelines for External Reviews developed by the Green and Social Bond Principles, of its actual performance level against each SPT for each KPI. The verification shall be conducted with limited assurance by the external reviewer(s).” The verification will be made public “no later than 120 days after each calendar year-end.

[x] https://hmgroup.com/wp-content/uploads/2020/10/HM-Group-Sustainability-Performance-Report-2019.pdf

![]()

This work is licensed under the Creative Commons Attribution-NonCommercial-