EU Regulation to cause log jam in commodity flows:

Financial Institutions are potentially in scope at first review

Please see the Investors’ Engagement Sheet here.

Deforestation regulation in the EU is likely to be adopted in the next 12 months requiring EU importers to confirm that cattle, cocoa, coffee, oil palm, rubber, soya, wood and derived products are deforestation-free. China, Brazil and Indonesia are the biggest non-EU exporters of commodities covered by the Regulation. China mostly exports wood and wood-derived products, Brazil soya and coffee and Indonesia palm oil. As a percentage of total exports China, Brazil and Indonesia are also the largest countries to be subject to the Regulation.

The impacts are likely two-fold. Firstly, this Regulation asks a major question of importing corporates as to whether they have traceability within their supply chains. Secondly, it has the potential to disrupt corporates which do not have traceability and responsible sourcing embedded within their supply chain.

EU deforestation regulation is coming down the pipe

Prior to the start of the milestone Conference on Biodiversity (COP15), on 5th December 2022, the European Council and Parliament announced a provisional political agreement on the new EU deforestation-free supply chains Regulation.1

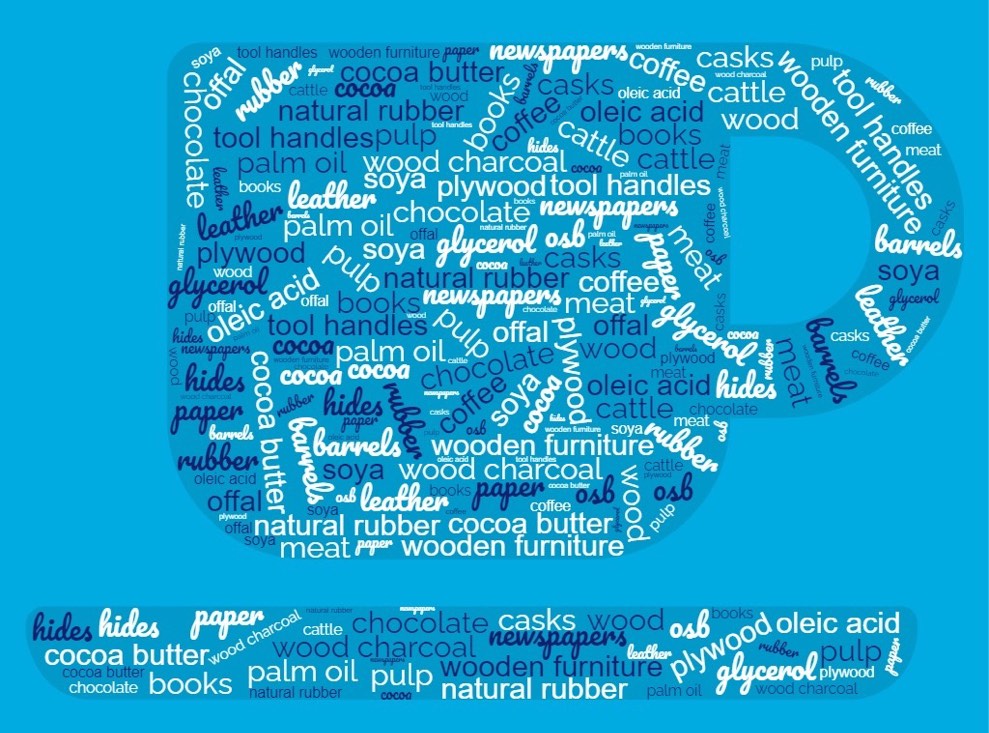

The aim is to reduce global deforestation and forest degradation that is caused by consumption within the EU. It is based on a mandatory due diligence scheme to be carried out by companies that import or export deforestation-linked commodities. Specifically, the regulation refers to cattle, cocoa, coffee, oil palm, rubber, soya and wood as well as derived products, such as beef, furniture or chocolate, as illustrated by Figure 1 (see the complete list in annex I of the full draft Regulation).

This Regulation requires the aforementioned products to be accompanied by a due diligence statement, containing the origin of production down to geo-location co-ordinates of plots of land. After carrying out the risk assessment, importers assume responsibility for the sourcing of the product. The product is then benchmarked to ascertain the risk of the product being linked to deforestation (high, standard or low). The benchmarking system will be updated periodically to reflect changes in production patterns.

The commodities and derivatives that will be impacted

Planet Tracker analysed trade data from Comtrade for the last 5 years (2016-2020), as processed by CEPII in the BACI dataset.2

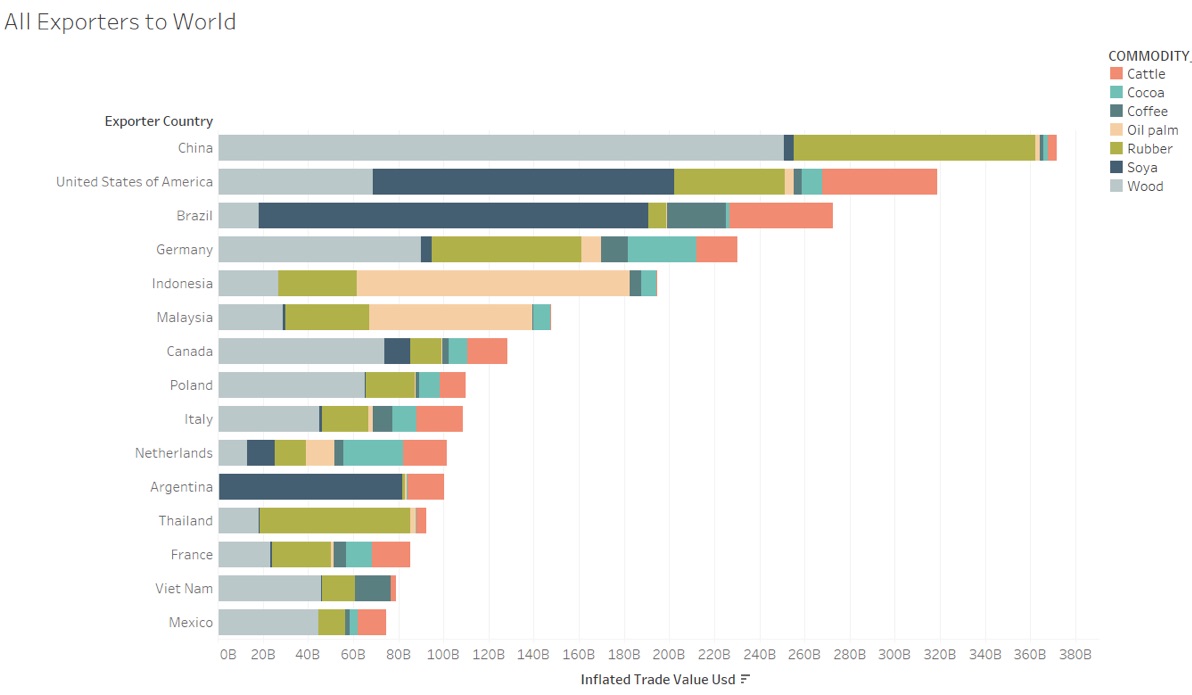

Figure 2 shows the top exporters of such commodities to the world. China (USD 370 billion), USA (USD 319 billion) and Brazil (USD 273 billion) top the list of countries.

Figure 2: Top exporters of deforestation linked commodities, as defined by the EU regulation, globally. Trade value of exports from 2016 to 2020, inflated to 2020 USD. Derived from Comtrade data.

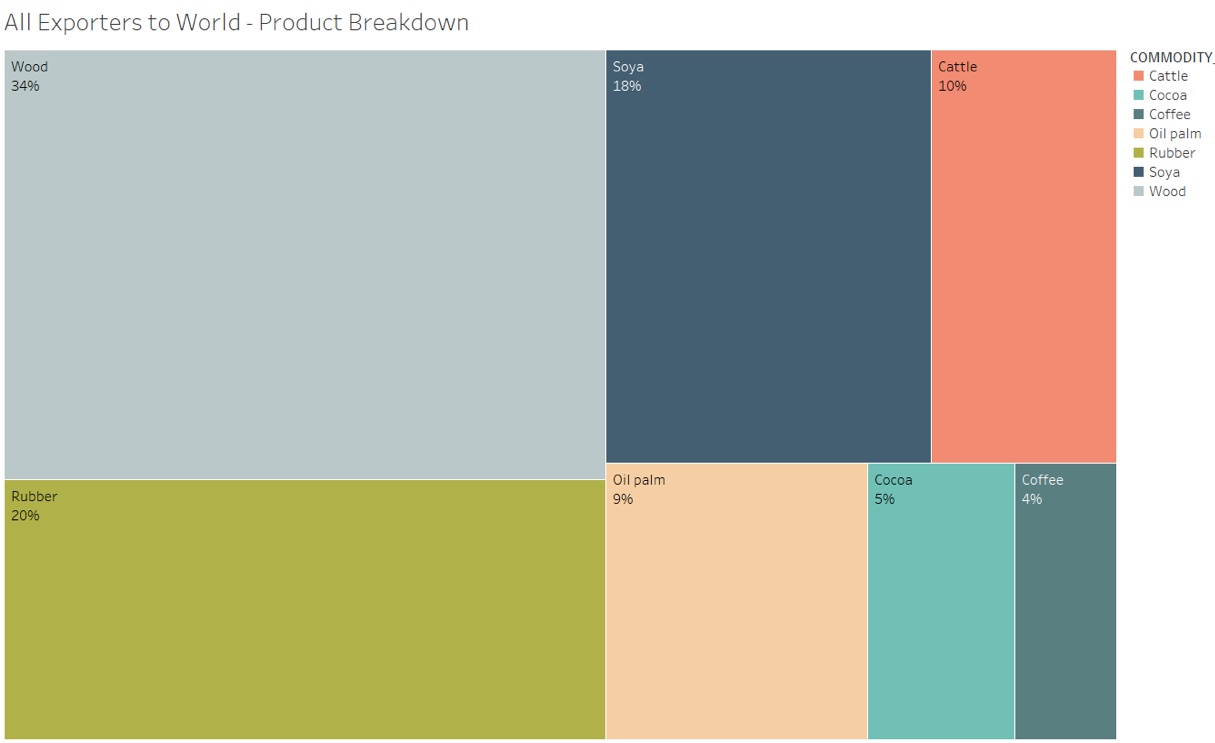

Wood and wood-derived products are the largest commodity, followed by rubber and soya, as can be seen in Figure 3.

Figure 3. Product breakdown of the top 15 exporters from Figure 2 above. Trade value of exports from 2016 to 2020, inflated to 2020 USD. Derived from Comtrade data.

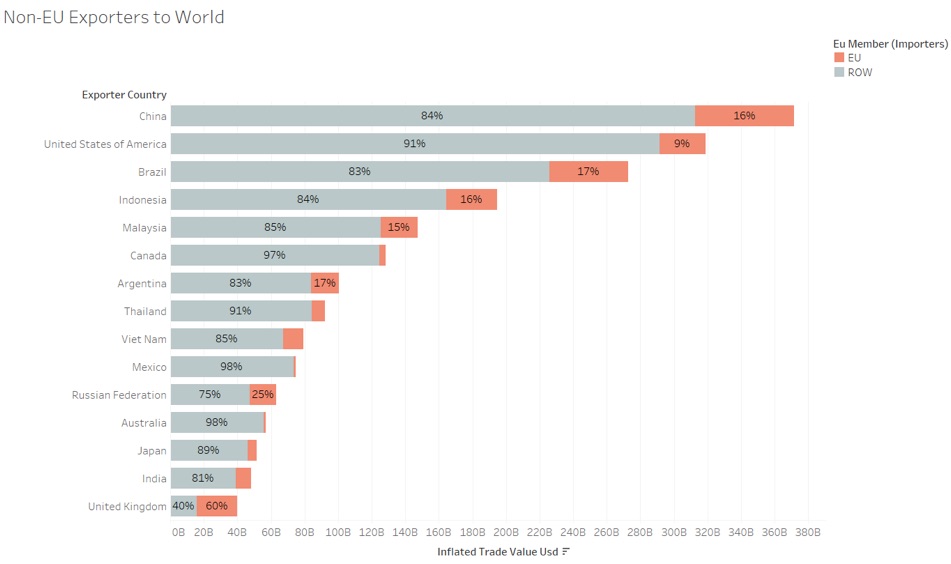

Filtering for non-EU exporters, Figure 4 shows that the majority of the resulting list of countries’ exports are not to the EU. However, the amounts exported to the EU are still material: China for example, exports USD 59 billion to the EU, which is 16% of the USD 372 billion of its global exports of the listed commodities.

Figure 4: Top exporters of deforestation linked commoditities to the EU, excluding EU countries, broken out by exporting to EU and ROW. Trade value of exports from 2016 to 2020, inflated to 2020 USD. Derived from Comtrade data.

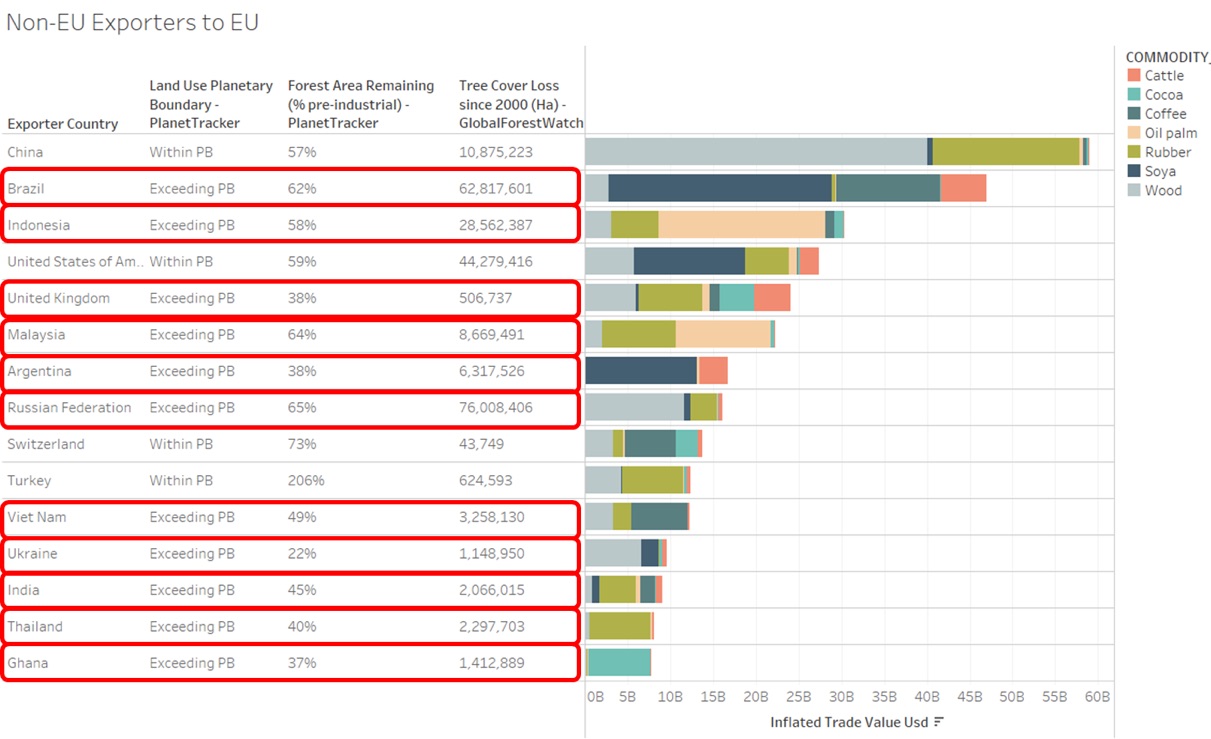

Figure 5 shows the top non-EU countries exporting to the EU market, broken down by commodities. These are the trade flows most likely to be affected by the draft Regulation. The top 3 exporters are China (USD 59 billion), Brazil (USD 47 billion), and Indonesia (USD 30 billion). China mostly exports wood and wood-derived products, Brazil exports soya and coffee, and Indonesia exports palm oil . As a percentage of total exports China, Brazil, and Indonesia are the largest countries to be subject to the regulation.

Figure 5 overlays deforestation statistics. Since the definition of “deforestation risk” can differ across countries, and the EU is yet to publish the list of countries classified as “high risk”, three ways of identifying deforestation risk are included. The first column shows whether the country is within the Land-system Change Planetary Boundary (PB), as calculated by Planet Tracker. The second column shows the forest area remaining, as a percentage of the total forest area in the pre-industrial era. The third column shows total tree cover loss since 2000 as estimated by Global Forest Watch.

The Land-system Change Planetary Boundary sets a minimum percentage of forest cover for each of these forest types to ensure the stable ‘Earth System’ essential for humanity’s survival in the long term. Land-system change is the recognized term for this boundary (used by the Stockholm Resilience Centre) and maintaining the extent of forests globally is a key component. These percentages should be used to guide the protection and restoration efforts of forest ecosystems. Tropical and boreal forest loss should not exceed 15% of original forest cover and temperate forest loss should not exceed 50%. 1700 is considered the pre-industrial benchmark for this methodology.3

Planet Tracker applied these forest planetary boundaries to each country, to produce our estimate of the planetary boundary for each country specifically. Figure 5 shows the combination of the planetary boundary work relating to forest area and the exports to the EU. In terms of exporters to the EU who are exceeding their land use change planetary boundaries Brazil, Indonesia and the UK are the largest. Notably since 2000, Brazil and Indonesia have seen continued significant forest lost. Since 2000 Russia has had the largest forest loss but given the current geopolitical situation, we expect Russian exports to the EU to drop off significantly, meaning this deforestation Regulation will have little impact.

Figure 5: Forest loss vs pre industrial levels and tree cover loss since 2000 along with Planet Tracker’s estimate as to whether it is within the Land-System Change Planetary Boundary. The bar chart shows trade value of exports from 2016 to 2020, inflated to 2020 USD. Derived from Comtrade data.

The Impact of the Regulation

Countries that will face the largest increase in due diligence requirements are China, Brazil and Indonesia based on the volume of exports to the EU. We have drawn this conclusion from Figure 4, where we can see these three countries are firstly significant exporters of deforestation linked commodities and secondly export a material percentage to the EU. Overlaying Figure 5’s analysis, we can see that Brazil and Indonesia are also two countries that have exceeded their planetary boundary in regards to land use change.

Further countries of note are Argentina (17%) and Malaysia (15%) whilst the UK, with a small amount of exports, has the highest percentage to the EU (60%).

The Regulation, in its draft format, is back-dated to 31st December 2020, to ensure that products linked to deforestation produced during the negotiation period are not allowed to be sold on the EU market or exported from the EU. The Regulation is expected to be adopted by the end of 2023. Once in place, operators and trading companies will have 18 months to implement the new rules. Micro and small enterprises will have a longer adaptation period – see Figure 6.

Figure 6: Timeline of the EU deforestation regulation implementation

The latest Forest 500 produced by Global Canopy shows that 31% of the 350 companies most exposed to deforestation risks do not have any policies for tackling the problem. Another 14% have some form of policy, but their target dates for ending deforestation in their supply chains lie well beyond the date when we expect the Regulation to take effect (mid-2025). This suggests that these companies will find it challenging to cope with the changes required by the forthcoming EU Regulation in the time allowed.

The requirement for attestation and transparency will allow 3rd parties, such as NGO’s and non-profits, to better interrogate supply chains. This increased interrogation should allow better tracing and identification of business practices supporting deforestation. Cattle laundering, the process of mixing cattle from deforested land with regular stock, is a key example of this. Following the implementation of this regulation, in our view, it will be possible to better highlight these practices and link them to a regulatory violation. This will, in theory, allow lawsuits and penalties to be brought for proven violators. The increased transparency and regulatory pathway for penalties will, in our view, allow markets to better self-regulate.

After two years, the Regulation will be reviewed, possibly expanding it to financial institutions (FI’s) and other types of products4. Whilst the current regulation doesn’t contain any reference to FI’s funding deforestation, there are calls for this to be changed at the first review.5This could mean that by 2025 there is regulation requiring FI’s to prove they are not funding deforestation. The Forest 500 report shows that 61% of the financial institutions most exposed to deforestation risk through their lending or investments do not have a deforestation risk policy so are unprepared for any such change in the law. This would put further pressure on potential violators and provide a recourse route to penalising those funding deforestation and land use change.

Summary

In conclusion, the deforestation Regulation is likely to be adopted in the next 12 months requiring the specific commodities to be deforestation-free. China, Brazil and Indonesia are the biggest non-EU exporters of commodities covered by the regulation. Brazil and Indonesia, based our analysis, are the most exposed as they appear to be already exceeding their forest cover planetary boundaries.

The impacts are likely to be two-fold, firstly, this regulation asks a major question of importing corporates as to whether they have traceability within their supply chains and whether that has been in place since 31st December 2020. Secondly, it has the potential to disrupt the corporate supply chains of those which do not have traceability and responsible sourcing embedded (and it is clear that many companies exposed to this risk are unprepared to tackle deforestation).

Looking ahead, there have been calls for FI’s to be included within the regulation and this is a possibility at the first review in two years (2025).6 This will put further pressure on potential violators and provide recourse and liability to those funding deforestation and land use change.

![]()

This blog is funded in part by the Gordon and Betty Moore Foundation through the Finance Hub, which was created to advance sustainable finance.

This blog is funded in part by the Gordon and Betty Moore Foundation through the Finance Hub, which was created to advance sustainable finance.

1 Regulations full name: Regulation on the making available on the European Union market as well as export from European Union of certain commodities and products associated with deforestation and forest degradation. The full draft regulation: https://data.consilium.europa.eu/doc/document/ST-16298-2022-INIT/EN/pdf

2 CEPII – BACI

3 Steffen et al. (2015) Planetary boundaries: Guiding human development on a changing planet. Science.

4 https://ec.europa.eu/commission/presscorner/detail/en/ip_22_7444

5 Banks escape EU due diligence obligation on deforestation, again – EURACTIV.com

6 Banks escape EU due diligence obligation on deforestation, again – EURACTIV.com