Increased soy certification would decrease deforestation risk

Planet Tracker believes supply chain traceability and transparency are essential to achieve Deforestation and Conversion-Free (DCF) soy supply chains. A strong certification system would help but soy lags behind other deforestation-linked commodities in this respect.

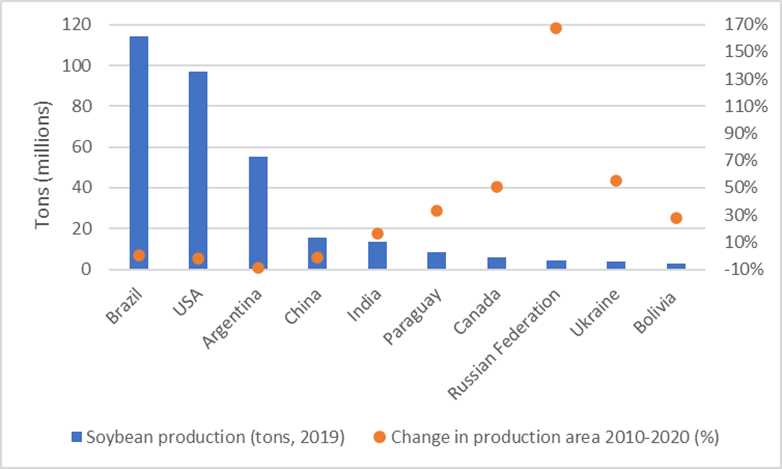

Figure 1: Top ten soy producers globally.1

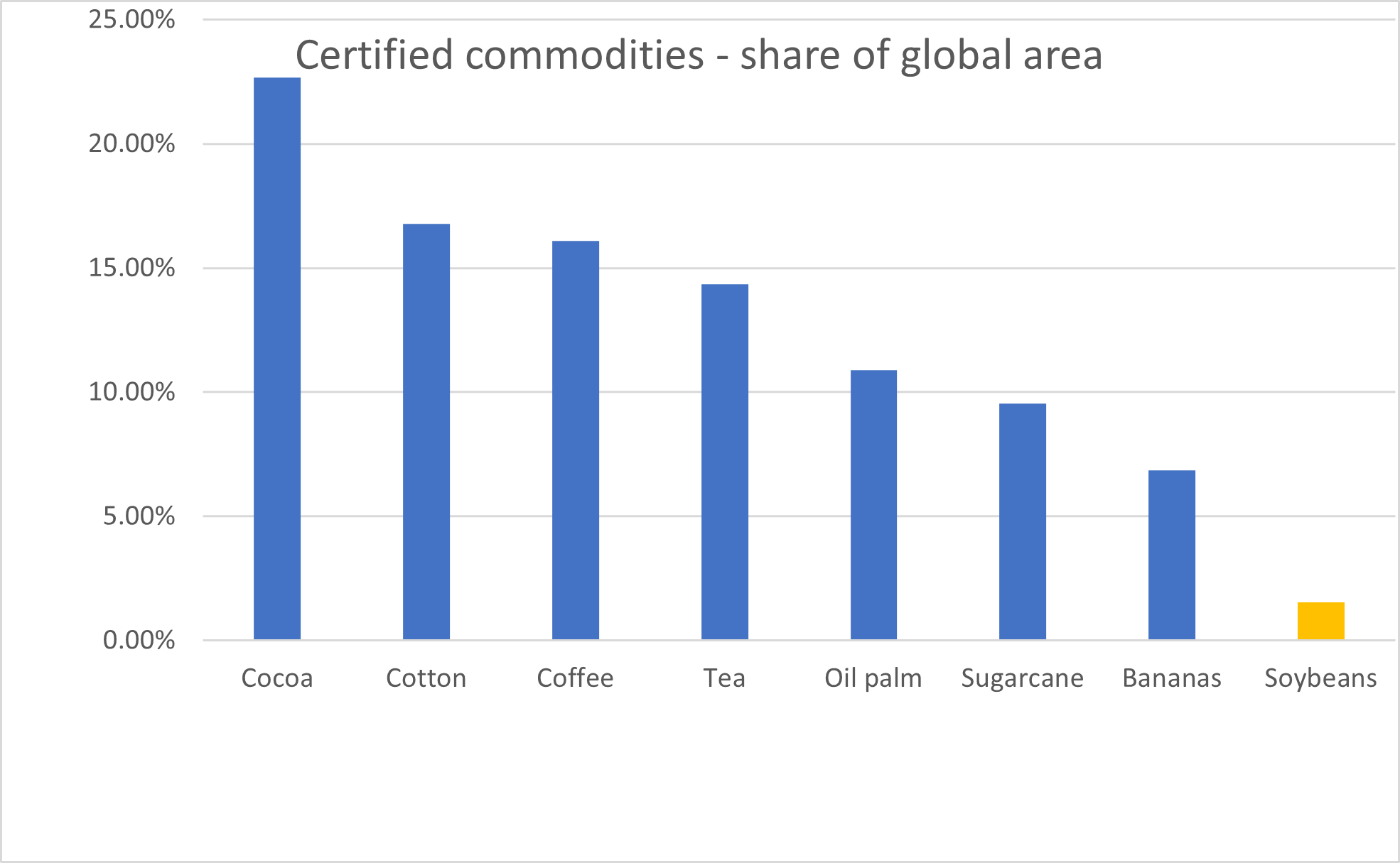

Certified soy amounts to c.3% of total soy volumes globally in 2020.2 This is very low versus other deforestation linked commodities. The ‘State of Sustainable Markets 2021’ report, published by the International Trade Centre, compares certification rates across various commodities and shows soy as the clear laggard – see Figure 2.3

Figure 2: Comparison of commodity certification rates (share of global production area certified)

Source: FiBL-ITC-SSI survey 2021 – figures quoted are minimum values for 2019 and only cover selected certification systems.

Soy has lagged behind other commodities, in our opinion, for three reasons:

- Soy has lower consumer exposure & awareness versus other deforestation-related commodities. It rarely appears on labels or on the back of packaging in the EU as for example, 90% of EU imported soy is used for livestock feed.

- A proliferation of certification systems has limited the scale any one certification can achieve.5 Whereas in palm oil the RSPO (Roundtable on Sustainable Palm Oil) is by far the largest certifier – that leadership and critical mass has not been achieved in soy.

- Partly related to the first point, there is limited demand for certified soy from further down the supply chain. In our conversations with certifiers and traders there is willingness to increase certified volumes, but without demand from further down the supply chain there is no way to spread the costs of certification. Farmers have little incentive to complete the certification process if there is not the demand and therefore a premium for certified soy. From our discussions with certifiers the premium, driven by market dynamics, is rarely enough to cover the costs of certification.

FEFAC6, which describes itself as the voice of the European compound feed & premix industry, has guidelines on soy sourcing. Unfortunately, a large number (c.20) of certifications meet the FEFAC guidelines and so are acceptable, contributing to the fragmentation of the certification industry. Since it represents one of the largest buyers of South American soy, FEFAC should be helping to build scale around a small number of best-in-class certifications and driving up demand for certified soy.

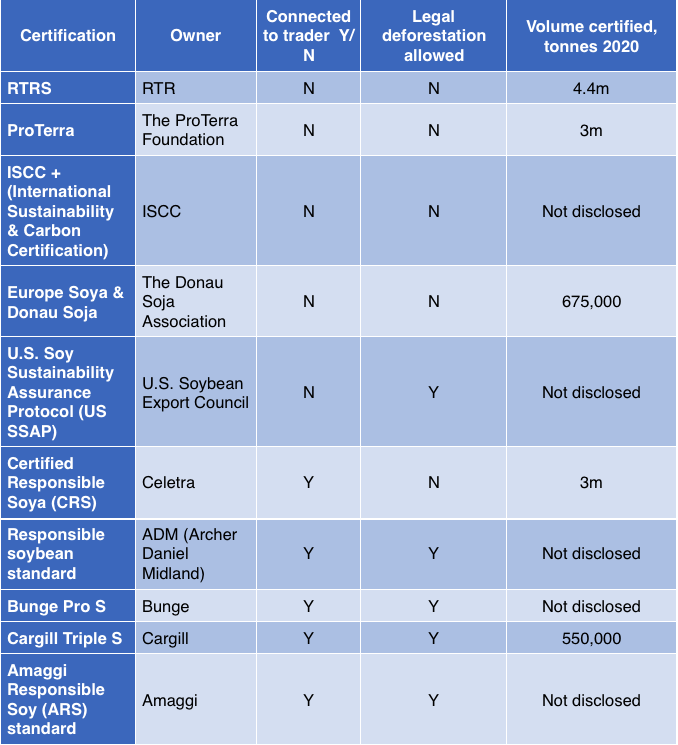

What certifications are there for Soy?

There are around 70 soy certifications. The ten listed below6 are only a sample, but we believe it captures the most significant.

There are significant challenges associated with analysing these certification systems:

- There is limited transparency around certification volumes

- There is very limited information about the geographies and locations that are being certified

- There is limited (or no) information about the methods of certification used (see our appendix for methods), particularly when it comes to maintaining traceability of soy moving through the supply chain

Certification systems are often not independent

One major issue with many of the soy certification systems is that they are run by the soy traders themselves rather than an independent body creating very obvious conflicts of interest.

Table 1 below highlights the conflicts of interest, low requirements and poor disclosure in ten of the more significant certification systems.

Source: Planet Tracker research, EFECA Soy certification options, EFECA Standards Briefing 2020

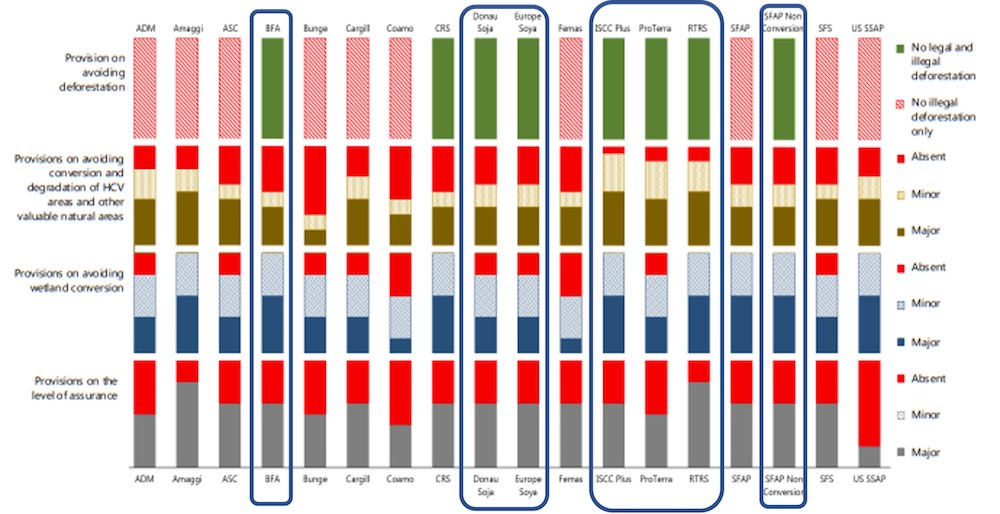

Kusumaningtyas, R. and Van Gelder, J.W. (2019, June) compared soy certification systems based on a number of criteria – unsurprisingly the independents scored more highly than the traders – see Figure 3.

Figure 3.: Comparison of 18 major soy certification programs (significant independent systems highlighted)

Source: Kusumaningtyas, R. and Van Gelder, J.W. (2019, June), Setting the bar for deforestation-free soy in Europe; A benchmark to assess the suitability of voluntary standard systems, Amsterdam, The Netherlands: Profundo.

RTRS – the best in a fragmented and murky industry

From our research the RTRS scheme emerges as the best standard in soy certification whilst also being one of the largest certifiers. It is worth noting that Proterra also consistently scores highly. Across the board the independent certifiers, i.e. those that are not also traders, generally score higher than certifications linked to trading operations.

There have been criticisms levelled at the credit trading scheme that the RTRS offers – the detachment of the certification and the physical soy allows for purchasers to buy deforestation linked soy whilst claiming certification (for more details on this please see the appendix). This has been stated to be a transitionary process, aiming to make certification costs lower and to increase scale. Scale is something that the soy certification industry badly needs.

Why should investors care about certified soy?

The threat of EU regulation

The European Commission proposed a new Regulation on 17 November 2021 to restrict deforestation-linked products from entering the EU, ultimately banning the import of deforestation-linked soy. The proposed regulation will target six commodities linked to deforestation – coffee, cocoa, cattle, palm oil, soy and wood. It includes legal and illegal deforestation and requires strict traceability on all commodities.

This proposed regulation will work collectively with the existing Renewable Energy Directive, which regulates commodities used as biofuels (including derivatives of soy) to ensure the products used have not been harvested from areas which have undergone deforestation. This regulation provides a direct risk to earnings and so should be high on investors’ agendas when engaging with exposed companies.10 For further detail, please see prediction five from our ‘Seven Capital Market Trends to Watch in 2022’ blog.

In terms of investor engagement, there has only been one successful proposal to report on ‘eliminating native vegetation conversion in its soy supply chain’ (passed at Bunge’s 2021 AGM). Prior to that there have been 18 proposals on deforestation from 2012 to 2020. Six failed and one passed; for the rest the companies did not disclose the results. The successful proposal was at P&G in 2020 to report on efforts to eliminate deforestation within their supply chain. Failed proposals were at Domino’s Pizza (2016 and 2017), DuPont (2016), Mondelez (2019), Yum! Brands (2019) and Restaurant Brands International (2019).11

The risk of a carbon tax on embedded emissions

Deforestation is a significant cause of CO2 emissions and so companies should be accounting for these emissions in their Scope 3 disclosures. By linking the deforestation data to carbon emissions and then to the soy export data we can estimate the CO2 emissions that are embedded in the soy imported into the EU. For further detail please see our report on the Gran Chaco: Deforestation Dozen.12 The European Commission has put forward a Carbon Border Adjustment Mechanism (CBAM) as part of its green taxation programme, which requires importers to buy digital certificates representing the tonnage of carbon dioxide emissions embedded in the goods they import.

The price of the certificates will be based on the average price of permits auctioned each week in the EU carbon market. It will be phased in gradually and will initially apply only to a selected number of goods at high risk of carbon leakage: iron and steel, cement, fertiliser, aluminium and electricity generation (from 2023). In 2026, it is expected to be fully operational and the EU will consider whether to extend its scope to more products and services. Given the heavy carbon footprint of deforestation there is a strong risk that soy (and similar imports) will be caught by an expanded CBAM.

Supply chain traceability is the key – but certification could be an important supporting tool

Companies that do not have full visibility over their supply chains cannot fully control or mitigate the environmental and reputational risks they face. However, buying soy that has been certified as deforestation-free by an independent certifier is a simple (interim) step for companies to take.

And ‘what proportion of your purchased soy is credibly certified?’ is a simple question for investors to ask their investee companies.

Methods for the chain of custody certification

There are numerous methods of certification with varying outcomes and costs. Certifiers often don’t make it clear which method has been used and how the certification is assured through the value chain.

Book & Claim (certificate trading): this is a credit trading platform that provides negotiable certificates of a certified product. The purchase of the physical product and the purchase of the certificate are separate and can happen independently.

Mass Balance: certified and non-certified products are mixed at any point in the supply chain. An administrative trail ensures that the output of certified soy delivered to customers does not exceed the input of certified soy received at the upstream location.

Area or group mass balance: a supply chain model that combines criteria from the mass balance and the book & claim systems. The raw material comes from certified sources located in specific areas and is followed administratively through the supply chain via a mass balance approach. Purchasers can obtain credits directly from growers, provided that these growers operate in the same geographic area as the soy that is bought on the regular market.

Segregation: the customer knows that 100% of the relevant ingredient used consists of certified materials. Bulk Commodity Segregation: certified products coming from different sources can be mixed. Identity Preserved (IP): the certified product is physically separated from other products originating from other sources. IP is relevant for GM-free assurance.

Direct sourcing: an exception, but this involves direct trade commitments between farms producing certified soy and downstream companies.

Source: DH and IUCN NL (2019) European Soy Monitor. Researched by B. Kuepper and M. Riemersma of Profundo. Utrecht and Amsterdam: The Sustainable Trade Initiative and IUCN National Committee of the Netherlands

Appendix

RTRS

The Round Table on Responsible Soy Association (RTRS) is the largest certifier of soy. RTRS certified 4.4 million tonnes of soy in 202013, this relates to 1.2 m ha and 9,536 farms.

Founded in 2006 in Zürich, the RTRS is a non-profit organisation committed to promoting the production, trade and use of responsible soy consisting of over 180 members. The RTRS aims to ensure “current and future soybean is produced in a responsible manner to reduce social and environmental impacts while maintaining or improving the economic status for the producer”.

The RTRS has two certification standards: The Standard for Responsible Soy Production – aimed at soy production, and The Chain of Custody Standard – aimed at the soy value chain.

The RTRS abides by five key principles in their aim for responsible soy, these include:

- Legal Compliance and good business practices.

- Responsible labour conditions.

- Responsible community relations.

- Environmental responsibility.

- Adequate agricultural practices.

The RTRS initiative relies mostly on the trade of ‘RTRS credits’. In 2021, 4.25m tonnes (of the 4.4m certified tonnes) of RTRS credits were purchased by external companies.14 The RTRS grants one credit to certified producers for every tonne of sustainable soy produced. These credits are then commercialised independently from the physical soy and can be exchanged on the RTRS trading platform. This payment is separate to the payment for the soy which cannot be sold as certified once a credit payment has been received. The credit allows manufacturers and users of soy to pay the producers directly for their certification whilst removing the expense of segregating the beans.

1 Food and Agriculture Organization of the United Nations (FAO) 2021. https://www.fao.org/faostat/en/#home

2 4.4m + 3m + 3m + 0.55m + 0.675m (2020) /348.71m (2018, source: https://ourworldindata.org/soy

3 The State of Sustainable Markets 2021, ITC https://intracen.org/resources/publications/the-state-of-sustainable-markets-2021

5 Commentary from RTRS

7 In our discussions with certifiers, we heard estimates of ‘around 70 certification systems’

8 Selected from our research including but not limited to EFECA

10 Regulation of the European Parliament and of the Council on the making available on the Union market as well as export from the Union of certain commodities and products associated with deforestation and forest degradation and repealing Regulation (EU) No 995/2010.

11 Insight Proxy (2022)

13 https://responsiblesoy.org/impacto?lang=en#impacto

14 https://responsiblesoy.org/compradores-de-creditos-rtrs?lang=en