Beached, not Stranded

Shipbreaking in Chattogram, Bangladesh

On World Ocean Day, Planet Tracker investigates the fate of fishing vessels that are past their ’use by’ date. Between 2014 and 2020, fishing vessels responsible for an estimated 1% of global wild-catch volumes have been dismantled. In tonnage terms, 55% of them can be traced back to Russian companies. Half of these vessels were beached (i.e., deliberately laid ashore) and broken down in India or Bangladesh, with a dreadful environmental and human impact. We expect more beached fishing vessels in coming years, mainly due to the growing age of global fishing fleets, which ensures a low ‘stranded asset‘ risk (obsolete vessels retired prematurely) in the fishing industry. By conditioning funding to the implementation of strict decommissioning policies, investors and lenders can mitigate the environmental and human impact of the future growth in beached fishing vessels.

More ships for less fish – are fishing vessels at risk of being stranded?

Between 1950 and 2015, the number of motorised fishing vessels increased sevenfold globally. In the same period, wild-catch production ‘only’ quadrupled.[i] This discrepancy cannot be explained by a significant shift in the average size of vessels (the number of vessels with power below and above 200kW both rose sevenfold over the period),[ii] but instead by a decrease in catch per unit effort (CPUE) – i.e. total wild catch divided by the total amount of effort[1] used to harvest the catch. Over the same period, with fish stocks overfished, CPUE has decreased by over 80% in most countries.[iii]

What are the implied risks for the global fishing fleet? Are ‘stranded assets’ – assets that have suffered from an unanticipated or premature write-down, devaluation or conversion to liabilities – about to become a reality in the fishing vessel industry? Planet Tracker investigated, focusing on the fate of decommissioned and scrapped fishing vessels.

From Russia with laws

Using data from The Shipbreaking Platform,[iv] we analysed the country of beneficial ownership of the fishing vessels scrapped, their flag states and the location of their dismantling. Overall, between 2014 and 2020, Planet Tracker computes that fishing vessels with a cumulative gross tonnage of at least 219,000 tonnes have been dismantled and therefore removed from the oceans.[v] These vessels would have caught around one million tonnes of seafood between them every year, equivalent to about 1% of global wild-catch production.[vi]

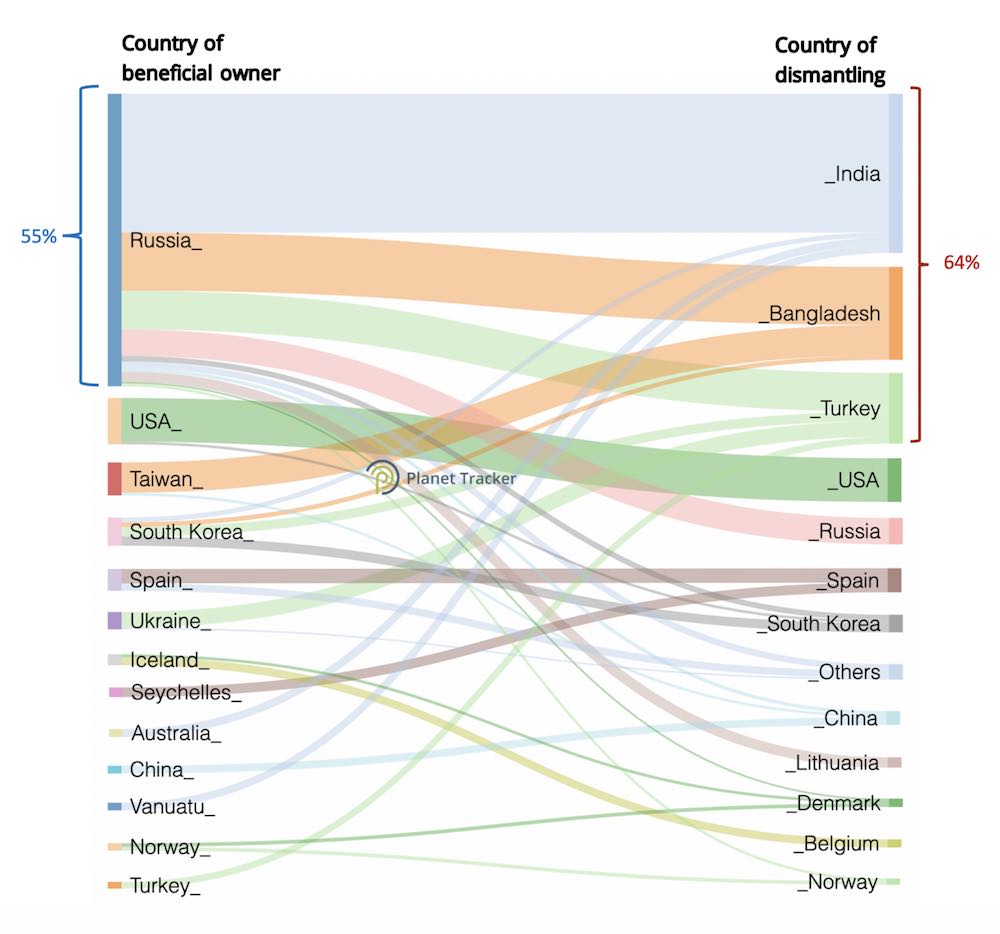

In tonnage terms, 55% of the fishing vessels dismantled between 2014 and 2020 can be traced back to Russian companies.[vii] 75% belonged to either Russian, American, Taiwanese or South Korean companies.[viii]

The preponderance of Russian ownership among dismantled vessels is explained by Russia’s desire to modernise its fleet. The old age of the Russian fleet (28 years on average) prompted Russia’s Federal Agency for Fishery to launch incentives to spur fishing companies to renew their vessels. Between 2018 and 2030, half of the Russian fleet is expected to be renewed, and these vessels will have to be built domestically.[ix] In addition, Russia is expected to ban fishing vessels older than 30 years in 2033.[x] This should translate into growing numbers of scrapped Russian vessels in the future.

India, Bangladesh, Turkey: where fishing vessels go to die

Still in tonnage terms, half of the fishing vessels scrapped in 2014-2020 ended up in India and Bangladesh (two-thirds if we add Turkey) – see Figure 1.

Figure 1. Cumulative Gross Tonnage of Fishing Vessels Scrapped Between 2014 and 2020 by Country of Beneficial Owner (left) and Country of Dismantling (right) Ranked by Decreasing Gross Tonnage.[xi]

Fishing vessels dismantled in India or Bangladesh or Turkey typically belong to Russian, Taiwanese, Korean or Ukrainian companies.

Vessels whose beneficial owners are registered in EU countries are not generally sent to these three countries to be dismantled. This is because shipbreaking yards in India and Bangladesh are not on the list of approved facilities where ships sailing under an EU flag can be dismantled.[xii] There are two key reasons behind this: human and environmental costs.

The high human and environmental cost of beaching

The two key places where obsolete ships end their lives in these two countries are Alang-Sosiya in India and Chattogram (formerly known as Chittagong) in Bangladesh. There, they are beached (i.e. voluntarily grounded ashore), pulled apart and broken under rudimentary conditions on tidal mudflats.

Hazardous materials contained in the ships, as well as rust and metal remnants are dumped locally, contaminating the sands and sediments. Current and tides then distribute the pollutants, especially during the monsoon season. This affects marine life: near Chattogram in Bangladesh, 21 species of fish and crustacean have been wiped out by the local shipbreaking industry, which also endangered another 11 species.[xiii] Along a 14km coastal line, at least 60,000 mangrove trees have been cut to make way for more ships.[xiv]

The impact for the workers is very damaging too: blow-torch cutting exposes them to toxic fumes and explosions, falls, fires and suffocation are common. More than 1,000 people have died in shipbreaking yards in Bangladesh since the 1980s.[xv] In India, the incidence of fatal accidents (2 per 1,000 workers) dwarfs that in mining, considered to be very accident-prone (0.34 per 1,000 workers).[xvi]

Flags of convenience enable vessel owners to bypass legislation

In some cases, most likely to avoid the responsibilities linked to the scrapping of ships or their beaching in India or Bangladesh, fishing vessels change their flags before being dismantled. Table 1 shows a list of such fishing vessels.

Table 1. List of Fishing Vessels that Changed their Flags Prior to Being Scrapped (2013-2020).[xvii]

Interestingly, only one EU fishing vessel appears here. However, recent research showed that when considering all ships (not just fishing vessels), the vast majority of EU vessels being scrapped do use flags of convenience to bypass EU legislation on shipbreaking and are sent to India or Bangladesh.[xviii]

Overall, 26% of the gross tonnage and 19% of the fishing vessels dismantled between 2014 and 2020 sailed with flags of convenience, using the definition of flags of convenience established by the Environmental Justice Foundation.[xix] The five most common ones are Comoros, St Kitts and Nevis, Panama, Palau and Belize. Note that with the exception of Panama, all these countries are recognised as Small Islands Development States (SIDS) by UNESCO.

More beached fishing vessels ahead

When regulations are bypassed or loopholes exploited, the dismantling of fishing vessels has an unacceptable environmental and human cost. Unfortunately, our analysis shows this impact is likely to intensify in coming years.

The aggregate gross tonnage of the fishing vessels dismantled between 2014 and 2020 is equivalent to 1% of the estimated aggregate gross tonnage of the 2018 global fishing fleet,[xx] or about 0.15% a year. The real proportion is most likely higher, since the underlying data gathered by The Shipbreaking Platform relies on public information only and focuses on the largest vessels only – the smallest fishing vessel in the list has a gross tonnage of 250 tonnes. As a proportion of vessels with a gross tonnage of 250 tonnes or more,[xxi] this annual scrapping rate is 0.3% per annum in terms of number of vessels. This is not a high ratio: assuming that fishing vessels can last for 50 years and assuming a linear age distribution, the theoretical scrapping rate should be closer to 2%.

However, in 2019, the aggregate tonnage of fishing vessels dismantled was at the highest recorded level (47,463 tonnes).[xxii] In 2020, that record was beaten (50,586 tonnes).[xxiii] We would expect the proportion of fishing vessels to be decommissioned and dismantled to rise further, for two main reasons.

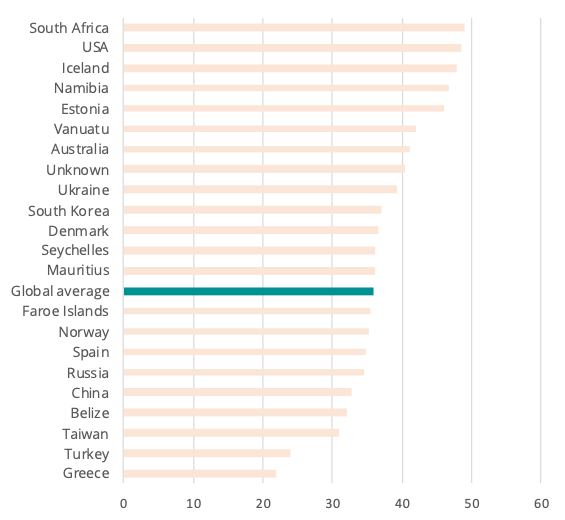

Firstly, the average age of the global fishing fleet has been steadily rising since the 1990s.[xxiv] It was 24 years in 2003 globally and is now significantly higher in many places, such as the US North Pacific (40 years),[xxv] Russia (28 years), or the Mediterranean and the Black Sea (29 years).[xxvi] As the average age of fishing fleets will become closer to the average age at which vessels are currently dismantled (36 years currently), more vessels are likely to be dismantled. In Russia for instance, the average age of dismantled fishing vessels is only six years above the age of the overall fleet – see Figure 2.[xxvii]

Figure 2. Average Age of Fishing Vessels Dismantled by Country of Beneficial Owner.[xxviii]

Secondly, growth in the size of the global fishing fleet has steadily slowed down having reached a peak in the 1970s. Between 2016 and 2018, the number of global motorised vessels shrank by an annual rate of 1.4%.[xxix] In 2018, there were 4.56 million fishing vessels traveling the oceans, of which 2.86 million were motorised.[xxx]

Minor risk of stranded assets

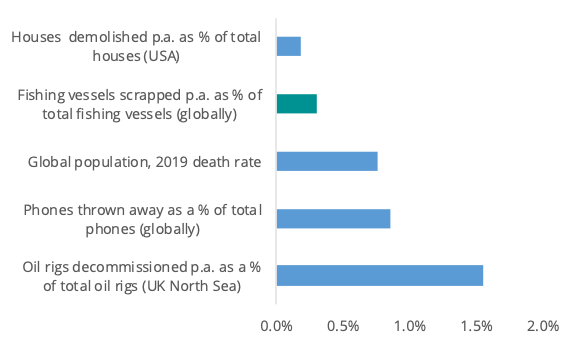

The current rate of dismantling of fishing vessels (0.3% p.a.) does not reveal any ongoing risk of stranding of such assets. In Figure 3 below, we compare this ratio to the decommissioning/death rate of:

- a stranded asset: oil rigs in the North Sea

- a high-longevity asset, with a marginal risk of being stranded: houses in the US

- a low-longevity asset, with a low risk of being stranded: mobile phones

- the global human population (for context- global average life expectancy: 73 years)[xxxi]

Figure 3. Putting the Annual ‘Death Rate’ of Fishing Vessels into Context.[xxxii]

Could this ‘stranded assets’ risk materialise in the future, as the rate of dismantling will accelerate? Not really, since it is very likely that in the context of ageing fleets, the fishing vessels being dismantled in the future will be the oldest ones. This means that they are likely to be fully depreciated and unlikely to be retired prematurely, and therefore do not fit the description of stranded assets.

Locally, young fishing fleets constituted of highly specialised vessels specifically targeting overfished species might still be stranded (i.e., retired prematurely), especially if they operate in enclosed seas and under lax environmental standards (making a sale, repurpose or transport of the vessel challenging). Yet we have no reason to expect this potential outcome to be widespread.

For this reason, and also because any potential stranded fishing vessels are likely to become beached vessels whilst beached ones are not typically stranded, a focus on beaching is perhaps more important.

What investors can do to limit the impact of beached fishing vessels

Why are vessels beached in India or Bangladesh to be broken down? Most likely, because it was estimated that ship recycling costs as much as USD 3-7 million more than ship breaking for the average ship owner.[xxxiii] Not all beaching is the same: sites where workers have proper safety equipment, operated with cranes and with limited risk of contaminating the surrounding environment are preferable to ones where workers break ships apart with blowtorches, unprotected, and with parts and pollutants contaminating the beach. However, beaching sites in South Asia (where the human and environmental impacts are the worst) are more profitable than elsewhere for vessel owners.[xxxiv]

This cost factor is also driving beaching behaviours amongst owners of small fishing vessels: for instance, hundreds of recreational fishing vessels are simply abandoned in areas such as Devon or Cornwall in the UK, where the cost of disposing of just one old fishing vessel is around GBP 50-75,000 for the local port authority. An estimated 130,000 recreational boats end their lives across Europe every year.[xxxv]

To limit the environmental and human cost of beached assets in the future, we urge investors to consider the following questions when engaging with owners of fishing vessels:

- What is the current decommissioning plan for the fishing fleet? How does it translate into company financials (e.g. provisions)?

- If such a plan includes beaching, where will it take place? What are the measures taken to ensure it is undertaken in a way that minimises human and environmental costs?

- Does the company have policies that ban the use of flags of convenience (to bypass tighter decommissioning and recycling requirements)?

Investors and lenders can then condition funds or offer preferential financing terms linked to the implementation of low-impact measures. For instance, owners of fishing vessels dismantled in EU-approved shipyards, or an equivalent list of facilities could be offered better financing terms than others.

Addressing the impact of the growing number of beached fishing vessels will be challenging. The first step for investors and lenders in the fishing industry is to realise the magnitude, complexity and growing importance of the issue. As fishing fleets across the world age and as their growth slows down, fishing vessels are unlikely to become stranded. Instead, and for the same reasons, they are likely to be beached. Beaching is already a reality, which destroys ecosystems and costs human lives.

[1] The time, fuel, vessels and other resources and inputs used to harvest the catch

[i] Planet Tracker calculations based on Rousseau, Watson et. al (2019). Evolution of global marine fishing fleets and the response of fished resources.

[ii] Planet Tracker calculations based on Rousseau, Watson et. al (2019). Evolution of global marine fishing fleets and the response of fished resources.

[iii] Rousseau, Watson et. al (2019). Evolution of global marine fishing fleets and the response of fished resources.

[iv] The Shipbreaking Platform data (2021)

[v] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[vi] Planet Tracker estimates based on SeaAround Us, FAO, and The Shipbreaking Platform

[vii] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[viii] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[ix] https://www.seafoodsource.com/features/russia-using-aggressive-incentives-to-renew-its-fleet

[x] https://www.seafoodsource.com/news/supply-trade/russia-likely-to-limit-fleet-s-operating-life

[xi] Planet Tracker calculations and chart based on The Shipbreaking Platform data (2021). Note: the design of this chart was inspired by Wan et al. (2021). Ship scrappage records reveal disturbing environmental injustice.

[xii] https://shippingwatch.com/suppliers/article12674923.ece

[xiii] NGO Shipbreaking Platform.

[xiv] NGO Shipbreaking Platform.

[xv] YPSA (2021) via NGO Shipbreaking Platform.

[xvi] Toxics Watch Alliance via The Shipbreaking Platform (no date).

[xvii] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[xviii] Wan et al. (2021). Ship scrappage records reveal disturbing environmental injustice.

[xix] Planet Tracker calculations based on The Shipbreaking Platform (2021) and EJF. https://ejfoundation.org/resources/downloads/EJF-report-FoC-flags-of-convenience-2020.pdf

[xx] Planet Tracker (2021) based on FAO (2020). The State of World Fisheries and Aquaculture 2020 and OECD (2020). Fishing fleet.

[xxi] FAO (2021). Global Record of Fishing Vessels, Refrigerated Transport Vessels and Supply Vessels.

[xxii] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[xxiii] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[xxiv] FAO, Multiple sources.

[xxv] https://www.portseattle.org/sites/default/files/2018-03/Fleet%20Modernization%20Final%2011_11.pdf

[xxvi] http://www.fao.org/3/cb2429en/CB2429EN.pdf

[xxvii] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[xxviii] Planet Tracker calculations based on The Shipbreaking Platform data (2021)

[xxix] http://www.fao.org/3/ca9229en/online/ca9229en.html#chapter-1_1

[xxx] FAO (2020). The State of World Fisheries and Aquaculture 2020

[xxxi] United Nations (2020).

[xxxii] Planet Tracker calculations based on multiple sources (2021)

[xxxiii] The Norwegian Council on Ethics

[xxxiv] https://www.reuters.com/article/us-shipping-investment-beaching-insight-idUSKCN1IG0JC

[xxxv] https://www.bbc.co.uk/news/uk-england-cornwall-57232394