How to lend shares sustainably

Globally, financial regulators are quite rightly investigating sustainability claims made by asset managers. Investors have a right to know whether sustainable and ESG funds do exactly what it says on the tin. One easy check, before diving into the intricacies of the investment process, is to determine whether sustainable funds undertake securities lending and, if so, is it in a sustainable way? One way for asset managers to promote their sustainability credentials would be to become signatories to the Global Principles for Sustainable Securities Lending (Global PSSL).

Hidden away…

Many investors will be unaware of securities lending but may well have benefitted from this practice.

Securities lending is where the owner of a security (e.g., an asset manager on behalf of fund or ETF owners) transfers them temporarily to a borrower (e.g., a hedge fund). This allows the borrower to short the stock; it can also increase liquidity and leverage if desired. In return the borrower transfers or pledges collateral to the lender[i] – this may be other bonds, shares or cash for example – and pays a borrowing fee.[ii] This fee, net of administration and operational costs, is returned to fund holders. In the vast majority of cases this borrowing is short-term.

So, it’s a win-win? Only for some. Certainly, the fund manager will receive income from the borrowing fee which is returned to the investors in the fund. However, often the investor will not receive the full fee as the asset manager will charge for this service. BlackRock [BLK US] for example returns 62% of all securities lending revenue for funds in the UK, Eire and Luxembourg. BlackRock keeps the balance ‘which covers all operational costs’.[iii] Furthermore, there is a risk associated with this trade. If the borrower goes out of business before the securities are returned and the value of the collateral has fallen or the securities on loan have risen, then the fund is unlikely to be fully compensated. In such instances the asset manager and lending agent is ‘not liable for any losses associated with the re-investment activity’ as JP Morgan Asset Management [JPM US] makes clear.[iv] So, for the asset managers it is a win-win, but not necessarily for the fund or ETF investor.

…but worth the effort

Although securities lending and borrowing is not well known to many retail investors, the size of the business is significant. IHS Markit [MRKT US] estimates that global securities finance revenue – defined as the amount paid by borrowers to the beneficial owners of the securities – totaled USD 9.3 billion in 2020, a 7% decline on the previous year.[v] Another data provider, DataLend, estimated that the global securities industry generated USD 7.7 billion in 2020, also noting a decline on the previous year.[vi]

This implies that global securities finance revenue generated an estimated 2-3% of global asset management industry revenue, based on the Bolton Consulting Group industry revenue estimates.[vii] At the end of last year, lendable assets reached a new all-time high of nearly USD 30 trillion according to IHS,[viii] out of total assets of USD 100 trillion at the world’s 500 largest asset managers.[ix]

Asset managers use these revenues from securities lending programmes to boost fund returns and reduce the expense ratio – i.e.. stay competitive. An analysis by Brown Brother Harriman – the C-Suite Asset Manager Survey – suggests that asset managers are looking to further ‘boost their performance by optimising security lending’.[x]

The ESG part

So why should there be a sustainable or ESG scrutiny in securities lending in particular?

There are three main reasons. The first concern is around stewardship. When a fund or ETF lends a security, it also transfers the ownership title, meaning the voting rights are transferred to the borrower. The lending fund can no longer engage on issues raised at an AGM or in relation to executive pay, for example. Only when the securities are returned can the portfolio manager re-engage with the corporate.

The second issue is whether securities lending – which enables the borrower to short the company’s share price – is suitable for ESG funds. The Japanese Government Pension Investment Fund argued in 2019 that securities lending was ‘inconsistent with its responsibilities as a long-term investor’.[xi]

We have discussed this issue in greater detail in ‘Why sustainable investors should embrace shorting’ and point to the benefits of shorting such as leading to a more efficient market where misinformation and mispricing can be promptly rectified. Other benefits include improved market liquidity, facilitating hedging and other risk management activities.

Thirdly, the security lending industry is viewed as opaque which inevitably raises apprehension around the process and its benefits. It has been largely overlooked in the ESG debate.

The Global Principles for Sustainable Securities Lending (Global PSSL) has introduced a principle-based approach for securities lending and borrowing.[xii] It aims to ‘increase trust, confidence and transparency alongside advancing the integration of ESG’.[xiii]

There are nine Principles in total. These include generalist ones such as agreeing to align with global and regional sustainable finance agendas by co-operating with international organisations, regulators and other key stakeholders (Principle 1), as well as pledging to provide accurate information about sustainable securities lending approaches and activities (Principle 3). The specialist principles tackle more detailed issues such as ‘wherever possible, cash reinvestments should be made in securities that are consistent with the ESG compliant collateral basket at the issuer level’ (Principle 4) and ‘market participants should co-ordinate their voting policies internally and recognise their impact on revenue’ (Principle 7).

The signatories

As of 7 September 2021, there were seventeen signatories[xiv] to the Principles.

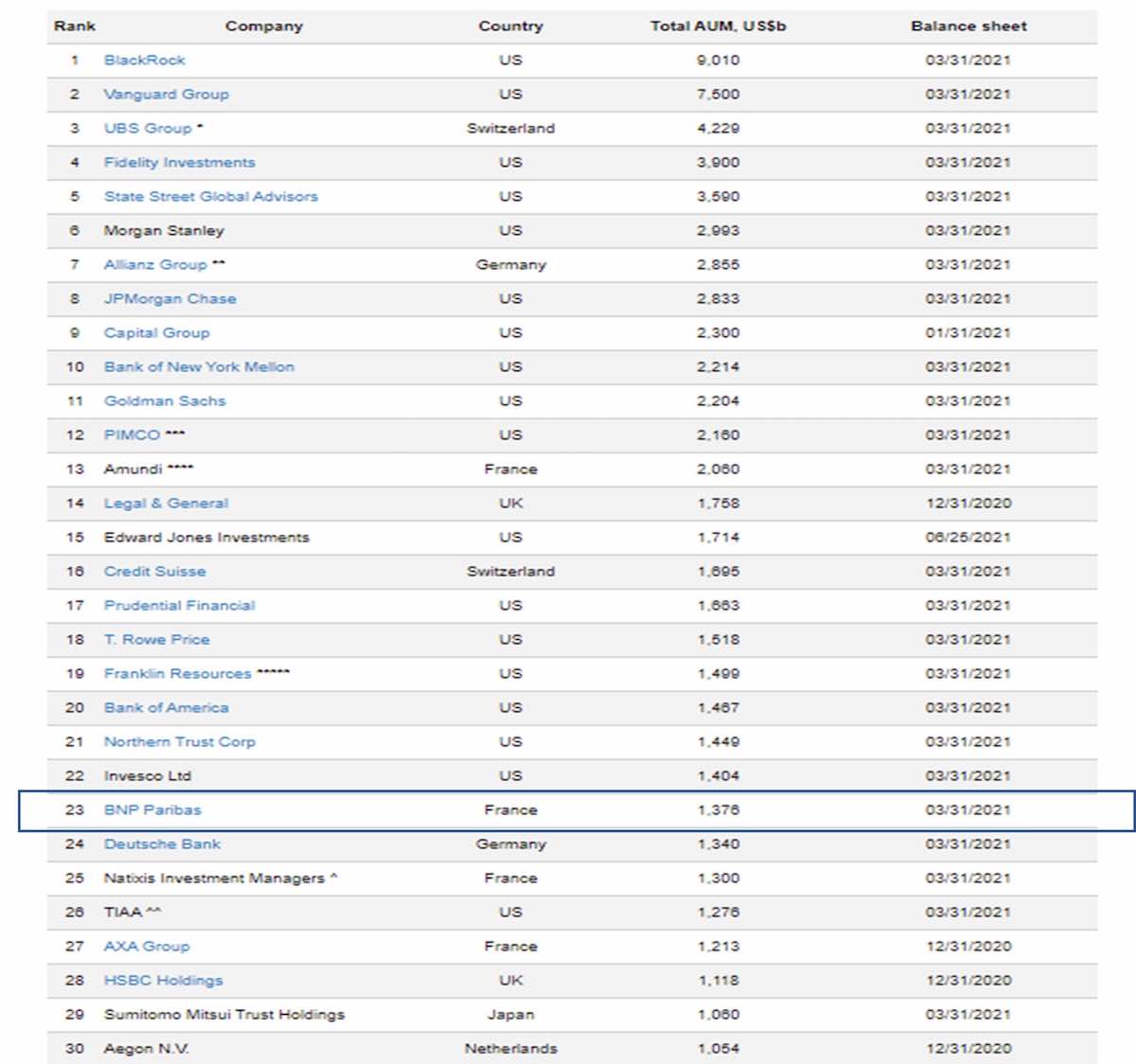

In Table 1, we rank the 30 largest asset managers globally. Only one organisation is a signatory of the Global PSSL: BNP, which is ranked 23rd by AuM (assets under management). However, to date it is BNP Paribas Securities Services which has signed rather than the asset management division. We recognise that we are showing the top asset managers ranked by all funds under management, not just sustainable or ESG assets, but these large investment firms promote sustainable and ESG investments.

Table 1: Top Global Asset Managers Ranked by Assets Under Management (AuM)[xv]

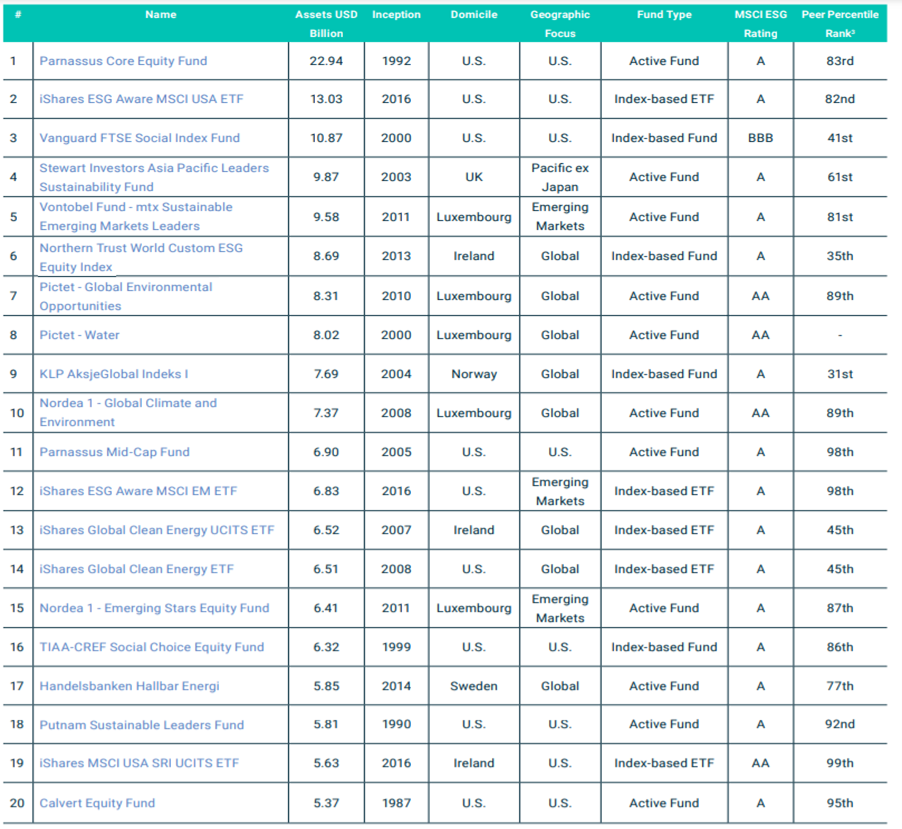

If we accept the MSCI definition of ESG funds, the Global PSSL sign-up still looks limited. MSCI ranked the top 20 ESG equity funds as at end December 2020 but recognised that ‘despite their nominal similarities these ESG funds vary widely in their manager’s investment approach and holding composition’[xvi] – see Table 2. Not one of these investment managers has signed the Global PSSL.

Table 2: Top 20 Largest ESG Equity Funds by AuM

Source: MSCI ESG Research LLC and Broadridge as of 31 Dec. 2020

Note that iShares is owned by BlackRock

The obvious next step

Those asset managers which manage sustainable funds on behalf of their clients should sign the Global PSSL if they undertake securities lending. These principles were submitted for consultation with the financial industry[xvii] and developed in collaboration with a group of financial firms ranging from pension funds and asset managers to data providers and hedge funds. Surely this is an obvious way for an asset manager to declare their sustainability credentials.

[i] The transfers that take place between the lender and borrower may involve a third party such as a prime broker or securities lending agent.

[ii] The cost of the borrowing can vary depending on the type of the security being borrowed. For example, it is cheaper to borrow large cap stocks than smaller ones. Furthermore, the lender may require a certain quality of collateral – e.g. a bond with a higher investment grade – which will increase costs if the borrower does not have them readily available.

[iii] https://www.blackrock.com/uk/individual/education/how-to-invest/securities-lending

[iv] https://am.jpmorgan.com/gr/en/asset-management/institutional/insights/securities-lending/

[v] https://cdn.ihsmarkit.com/www/pdf/0221/IHS-Markit-Securities-Finance-H2-2020-Review.pdf

[vi] https://www.prnewswire.com/in/news-releases/datalend-7-66-billion-in-revenue-generated-in-lender-to-broker-securities-lending-market-in-2020-825693586.html

[vii] https://web-assets.bcg.com/79/bf/d1d361854084a9624a0cbce3bf07/bcg-global-asset-management-2021-jul-2021.pdf

[viii] https://cdn.ihsmarkit.com/www/pdf/0221/IHS-Markit-Securities-Finance-H2-2020-Review.pdf

[ix] https://www.thinkingaheadinstitute.org/news/article/global-asset-manager-aum-tops-us100-trillion-for-the-first-time/

[x] https://www.bbh.com/us/en/insights/investor-services-insights/c-suite-asset-manager-survey.html

[xi] https://www.reuters.com/article/us-japan-gpif-idUSKBN1Y71F6

[xii] https://gpssl.org/revised-global-principles-for-sustainable-securities-lending-issued-alongside-opening-signatories/

[xiii] https://gpssl.org/wp-content/uploads/2021/07/Global-PSSL-draft-recommendations-transparent-value-chain-published-20-July-2021.pdf

[xiv] The 17 signatories are: Blue Orca Capital, BNP Paribas Securities Services, Breakout Point, eSecLending, Financial Decisions, FIS Global, J Capital Research USA, Minerva Analytics, Muddy Waters Capital LLC, Nest Corporation, NN IP, PGGM, Pierpoint Consulting, Sharegain, Standard Chartered, Sumitomo Mitsui Trust Bank, Quintessential Capital Management.

[xv] https://www.advratings.com/top-asset-management-firms

[xvi] https://www.msci.com/documents/1296102/24720517/Top-20-Largest-ESG-Funds.pdf

[xvii] https://gpssl.org/draft-global-pssl-undergo-public-peer-review/